The cut-off of gas supplies for Bulgaria and Poland on the 27th April 2022 exposed the risk of Russia restricting or fully stopping gas supplies to other EU nations, too, following its decision to demand payment in roubles from the 1st April. Gas flows to Europe accounted for 155bcm in 2021, or up to 40% of total European gas consumption. The loss of a part, or all that amount, would present a significant challenge for Europe

On March 8, the EU Commission published its REPowerEU plan, outlining measures to drastically reduce gas imports from their 2021 levels before the end of the year - and reach complete independence from Russian fossil fuels before the end of the decade. The key elements in this plan are diversifying supplies, reducing demand, and ramping up the production of green energy in the EU.

For Bulgaria, which is already affected by the gas cut-off, the focus is on securing alternative supplies, with the Energy Minister Alexander Nikolov indicating on the 5th May the country's willingness to cooperate with neighbours for joint gas purchases.

The majority of the 3bcm of natural gas is consumed in Bulgaria during the winter months for district heating. The year-round component of gas consumption is driven by the industrial sector, which uses natural gas both as a fuel and as a feedstock. The limited use of natural gas for power generation determines the negligible impact any switching in the power sector would have on total gas savings in Bulgaria.

In this analysis we look at the short-term possibilities of the overall European electricity market to reduce its gas demand in the period from 2022-2024 through a combination of fuel switch and delayed closures of thermal plants. We used our power despatch model to quantify the impact on the generation mix and emissions, as well as on gas demand.

Scenario set-up

We used our pan-European power model to estimate the potential that a radical gas saving policy would have on generation, emissions, and gas demand.

- Base Case: This is our current Q4 2021 Base Case, but updated to reflect current fuel prices and the significant reductions in expected French nuclear capacity in 2022 and 2023.

- Max Switch: This scenario is built on the Base Case but moves all gas plants to the right-hand end of the merit order. The scenario is intended to quantify the available switching to coal, lignite and oil that remains in the market if gas prices were to skyrocket in the event of a cut-off of Russian gas to Europe.

- Max Switch Additional Capacity: This scenario builds on the above, but assumes that Europe attempts to minimise its gas use in the power sector though bringing back some closed capacity and keeping plants online:

- Nuclear phase-out delayed in Germany and Belgium (+2GW 2023-2024).

- Lignite reserves utilised in Germany, and some coal brought back in GB and Italy (+4.6GW 2022-2024).

- All coal and lignite across Europe that is due to close this year and next instead keeps operating (+11.8GW in 2023, +18.8GW in 2024).

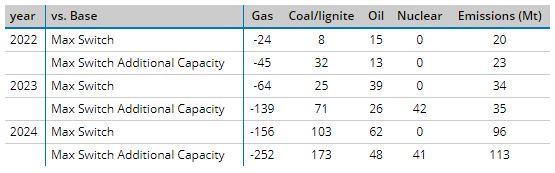

Results - generation and emissions

- For 2022, we took results starting from Week 10 (7 March) until the end of the year. The results show that there is minimal fuel switch away from gas left in the European system, amounting to +9TWh of coal/lignite and +15TWh of oil-fired generation, which enable a 24TWh reduction in gas generation across Europe for the rest of the year. Emissions would be 20Mt higher than the Base.

- In the Max Switch Additional Capacity scenario, there is slight increase in switching to coal as some plants are returned to the grid, which results in a 45TWh reduction in gas-fired generation. Emissions in this scenario ae 23Mt above the Base.

- For 2023, the Max Switch scenario leads to 64TWh reduction in gas-fired generation compared to the 2023 full-year Base. Coal and lignite account for 25TWh of fuel switch, while there is 39TWh of additional oil generation. Emissions would increase by a maximum of 34 Mt.

- However, the Max Switch Additional Capacity scenario sees a much more significant decrease in gas-fired generation (-139TWh compared to 2023 Base) due to the combination of delayed nuclear, coal and lignite plant closures. Emissions would only be 1Mt higher than the Max Switch scenario as the increased nuclear generation almost counteracts the higher emissions from coal, lignite, and oil plants.

- In 2024 the Max Switch scenario sees a substantial reduction of 156TWh in gas-fired generation compared to the 2024 Base, which reflects the fact that in the Base gas prices are expected to fall and incentive fuel switching back to gas-fired plants. Emissions are 96 Mt higher than the Base in this scenario.

- If coal, lignite, and nuclear phase-outs continue to be delayed, gas-fired generation is reduced by 252TWh compared to the 2024 Base, with emissions 113 Mt higher as coal, lignite and oil generation is maintained at high levels.

Results - gas demand savings

- In 2022, Europe would save 4.8bcm of gas for the remainder of the year if fuel switch potential was maxed out. In the Additional Capacity scenario this increases to 8.9bcm.

- For 2023 and 2024 our Base Case gas consumption increases as spreads encourage switching to gas at the same time as coal and lignite plants are phased out. To show the absolute rather than the relative savings in gas demand we therefore compare the results for these years to the 2022 Base Case:

- For 2023 the gas savings amount to 4.7bcm in the Max Switch scenario and 19.5bcm in the Additional Capacity scenario as delayed phase-outs of coal, lignite, and nuclear lead to further savings.

- For 2024, 7.6bcm of gas is saved in the Max Switch scenario, increasing to 26.7bcm in the Additional Capacity scenario.

- The results highlight that in the absence of new policy measures the power sector can do little to reduce gas demand in the short-term as fuel switch is already at elevated levels, meaning there is minimal prospects remaining even in an exceedingly high gas price scenario.

- For the remainder of 2022 only 4.8 bcm of gas could be saved though a full switch to coal, lignite, and oil.

- In this scenario, 26.7bcm of gas demand is saved by 2024, though it should be noted that this is an extreme scenario in assuming extremely high gas prices for 2.5 years.

While outside of the scope of this analysis it should be noted that the power sector can be a key driver of decreasing reliance on Russian gas in the mid- to long-term, through both switch from gas to renewables in the generation mix and electrification of gas-reliant heating and industry.

")