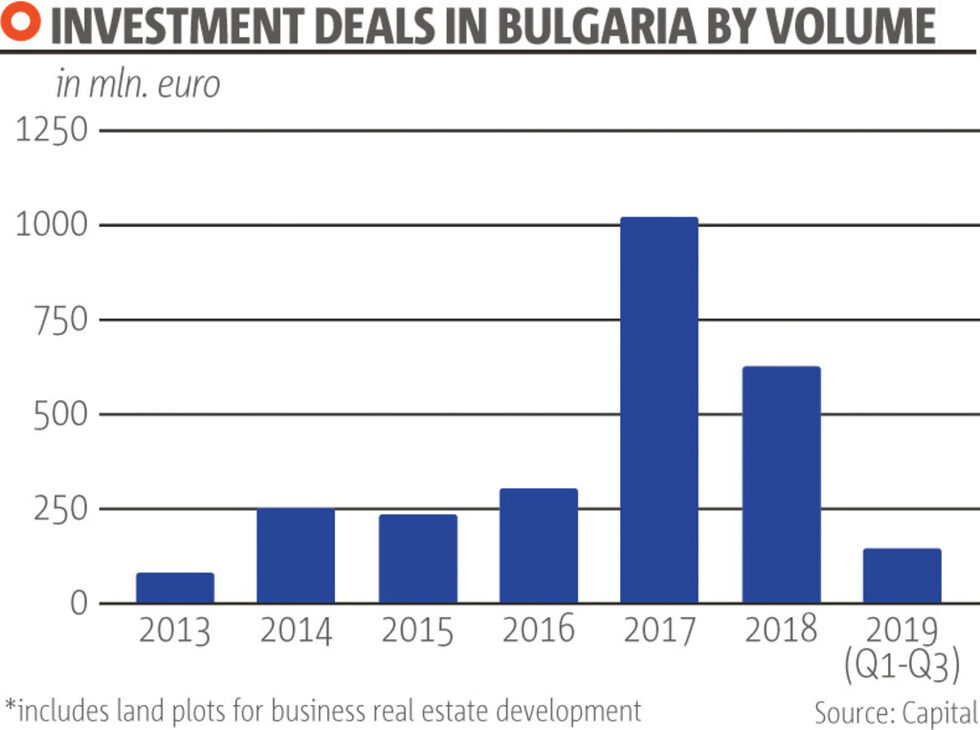

Business property deals in Bulgaria have sharply declined this year. The decrease for the first nine months is 74%, from 630 million euro in 2018 and even steeper when compared to the investment peak of 1 billion euro in 2017.

According to Cushman & Wakefield Forton real estate advisory firm, from January to September this year sales of business properties totalled 118 million euro, excluding the purchases of land parcels for construction. It is expected that the last quarter will traditionally be busier than the rest, but not enough to change the overall picture. In addition to the minuscule volume, the profile of the buyers is also alarming - there is a complete absence of big Western investors and total domination by local players.

"The reasons for the decrease are partially domestic: the lower liquidity of business properties in Bulgaria, the high expectations of the sellers and the country's dubious reputation earned over the years. But there are also global changes: the slower economic growth of the US, the Eurozone and Asian economies, the decreased industrial output in Europe," commented Mihaela Lashova, a managing partner at Cushman & Wakefield Forton.

7% drop in Europe, 74% in Bulgaria

The US consulting company Real Capital Analytics (RCA), which tracks the investment market for business properties, has reported a 12% average decrease in the volume of sales in Europe for the first three quarters in the three principal segments - offices, commercial and industrial spaces. The rise in alternative investments like hotels, apartment buildings and retirement homes (a new trend) has compensated to some extent for the 7% decrease in sales.

Even in the context of Europe's unfavourable environment, Bulgaria is not in good shape. It is part of the group of countries with the largest drop in investment sales (over 25%) together with countries experiencing political problems such as Turkey, the Ukraine and the UK, which is in the process of Brexit. There is also a decrease in small economies like Croatia and Slovakia - confirming the preference of large investment funds to invest in consolidated large assets instead of numerous small ones. There is also a more moderate drop of between 10% and 25% in Germany, Poland and Romania.

The regional business property investment champions with the growth of over 25% are the Czech Republic, where South Korean investors have entered the office building sector, and Greece and Italy, which are both chasing a previous slump. Serbia, which has a growing economy and a government that is in the habit of subsidizing construction companies, is also in that group despite not being an EU member.

Mihaela Lashova, a managing partner at Cushman & Wakefield Forton

Sellers have high expectations

The decreased sales volume of business properties in Bulgaria cannot be explained by the returns they yield. According to Cushman & Wakefield Forton, for first-class office spaces, the return is 7.5% - the highest in Central and Eastern Europe (CEE) where the average yield is 5.14%. Commercial spaces have an average return of 7.25% and industrial have 8.5%, as compared to 6.5% CEE average.

The absence of deals does not signify a complete lack of interest on the part of foreign investors. There is interest from funds that would purchase high return assets or problematic local assets that they could add value to, in addition to other smaller investors, Mihaela Lashova explains.

She believes that the sellers' attitude is the main problem. They have unrealistic price expectations as compared to 2017 and 2018. The prices they put forward generally squeeze potential returns by about a percentage point below what investors expect to be earning. The illiquid market additionally worries potential buyers.

Financing nuances

In spite of low-interest rates, a number of strings attached to financing in Bulgaria make the country less attractive than other destinations. "The returns on business property are 7-7.5% in Bulgaria and 4-4.5% in the Czech Republic. However, interest on financing is 1-1.5% there and 3% in Bulgaria. This means that the margin ends up being similar. At the same time, the market in the Czech Republic is a lot more liquid than in Bulgaria," explained Mihaela Lashova.

She adds that another problem in Bulgaria is the short-term nature of financing with a maximum span of 12-15 years, as opposed to up to 25 years in other EU countries. Furthermore, banks in Bulgaria retain the free cash of the borrowing company that remains after the scheduled payment has been made and use it for early repayment of the loan principal.

Bulgarian banks demand the borrower to cover 30-40% of project costs from its own funds and rarely automatic rollover of the loan. Western banks could allow zero amortization in case of such a significant rate of self-participation. This conservative approach has a considerable effect on investment returns.

The right product is missing

Additionally, supply in Bulgaria currently suffers from a lack of quality products that can be sold, Mihaela Lashova comments. The large shopping malls that created the volume of 1 billion euro in 2017 now have new owners. At the moment, they are investing in upgrades and are not in a selling mode. Some companies, like the South African fund NEPI, try to increase returns by developing new projects; in their case - a mall in Plovdiv. Another possible deal might involve two more malls, one in Varna and another in Burgas.

Iglika Yordanova, a managing partner at Collier's, also thinks that there has been a shift in investor interest: "In 2017 and 2018 the volumes in the investment market were generated by large assets, while currently there are few properties at over 150 million euro. Reselling within one or two years is not very typical. The absence of large properties for sale reflects on the reported volumes."

Parallel to this tendency, Colliers has observed that investors, foreign included, have expressed interest in vacant plots for development. This stimulates competition and creates an investment product for future deals, says Ignatova.

Office building forecast

There is a temporary lull in the availability of office buildings. If 2017 was the year of malls, 2018 was one of the office buildings. This year, there are deals for smaller, more problematic buildings often purchased from banks, in need of additional investment or restructuring in order to achieve higher occupancy. It is expected that the last quarter of the year will see the completion of several midsize office buildings. In the next three years, an additional 400 000 square meters of office space will go on the market, with the big wave expected to come in 2021. Some of the buildings have already been rented and the expectation is that this will create a new investment product and there will be deals.

The potential of industrial spaces

"Investors are also alarmed by the large volume of office spaces that are being built. Along with the fact that retail does not offer many investment opportunities, the last few years have seen increased interest in speculative projects in the industrial segment," Mihaela Lashova says. The present assessment of the market for industrial spaces (logistical and storage bases, industrial halls) is that it is insufficiently developed.

The available spaces are chiefly storehouses and bases for the company's own needs. According to Cushman & Wakefield Forton, from a total volume of about 1.2 million square meters, only 20-25% is intended for rent. There is an improvement in that respect. The owners of Industrial park Sofia-East and the East Ring logistical park, both based in Elin Pelin municipality, have plans for an expansion with the idea to offer more spaces for rent. Plans call for most of the space in the new project Logistical Park Sofia to be rented out as well.

At this stage, experts believe that the development of the industrial segment will focus on new projects, rather than investment deals. Another contributing factor is that in the last few years the pricing expectations of plot owners have become more realistic. Additionally, the breakthrough of several investors into the construction of utility infrastructure has given impetus to the development of entire regions. One good example is the logistical base of the household goods retailer Jysk in Bozhurishte, on the outskirts of Sofia, which has emerged as a location for furniture company warehouses and has two new projects underway.

This year, the Dutch company CTP, a prominent investor in industrial and logistical parks in CEE, came to Bulgaria with ambitious plans to build 100 000 square meters of space by 2021. "When an international operator enters the market it also brings along its corresponding international tenants, who express interest in the location. This allows for package rental deals for a group of countries, a model that is shared by commercial space owners," explains Lashova.

According to Lashova, a significant obstacle to the development of the segment in Bulgaria is that construction, land plot and infrastructure prices are higher than those in Poland, the Czech Republic, Hungary and Romania. Land suitable for construction costs 25-35 euro per square meter, but there are also prices in the 50-70 euro range. A further expense of at least 50 euro per square meter is required for the surrounding infrastructure. Additionally, the construction of a square meter of industrial space in Bulgaria costs 420-450 euro, while prices abroad are between 350 and 400 euro.

2019 - hotels for locals

The representatives of Cushman & Wakefield Forton have observed that there is real investment interest in acquiring brand hotels in Bulgaria from funds specializing in this sector. This happens against a backdrop of increased average occupancy and room rates, and in a market that is yet to be saturated with the brands of major international hotel chains.

"The return on hotel investments is currently in the 7-7.5% range. The unrealistic expectations of sellers reduce it to 6%. But foreign investors can acquire assets with the same returns in other Central and Eastern European countries, which makes this type of transaction redundant," Mihaela Lashova comments. She indicated that typically four- and five-star hotels are owned by Bulgarian investors who perceive them as the crown jewel of their businesses and that makes their price expectations unrealistic.

In the short term, there are no expectations for a major hotel investment purchase in Sofia. However, new five-star hotel projects will increase availability in the segment by 30%. Cushman & Wakefield Forton representatives have met with multiple foreign operators that have shown interest in entering the Bulgarian market, as long as there are investors that are willing to take on the risks and deliver a project that meets their standards. In addition to Sofia, smaller foreign operators have also expressed interest in building new projects in the ski resort of Bansko and on the Black Sea coast.

Expectations for 2020

If, after this soberingly slow year, sellers moderate their expectations, Bulgaria may see the return of deals, believes Mihaela Lashova. The absence of good investment projects is surmountable - especially with offices because new construction is picking up. But foreign investors' worries over the lack of liquidity are likely to remain. And in the negative scenario of a global slump, the market will continue to be small and driven by locals.

Business property deals in Bulgaria have sharply declined this year. The decrease for the first nine months is 74%, from 630 million euro in 2018 and even steeper when compared to the investment peak of 1 billion euro in 2017.

According to Cushman & Wakefield Forton real estate advisory firm, from January to September this year sales of business properties totalled 118 million euro, excluding the purchases of land parcels for construction. It is expected that the last quarter will traditionally be busier than the rest, but not enough to change the overall picture. In addition to the minuscule volume, the profile of the buyers is also alarming - there is a complete absence of big Western investors and total domination by local players.