![Fig.12: Total, male and female % of workforce with a tertiary level of education in Bulgaria [2000-2016]](https://kinsights.capital.bg/shimg/zx952y526_4149410.jpg)

Two labour components will affect the size of Bulgaria's economy and its growth rate on a 5-20 year horizon, the first is the number of employed workers in the labour force and the second is the productivity and contribution of that labour force including its total spending in the arena of consumption and services.

Assessing the first component, three factors from a demographic perspective can affect the number of employed workers in the labour force: 1) unemployment rates (a cyclical factor?), 2) the activity rate of the population (the economically-active population versus that total which could be economically-active) and 3) the total population that could be economically active.

The typical measurement of the population that "could be economically active" is the population between the ages of 15-64. This cohort of course includes students but as many of them work part-time and are (supposed to be!) acquiring knowledge and skills sets for future productivity, economists tend to include the whole age range.

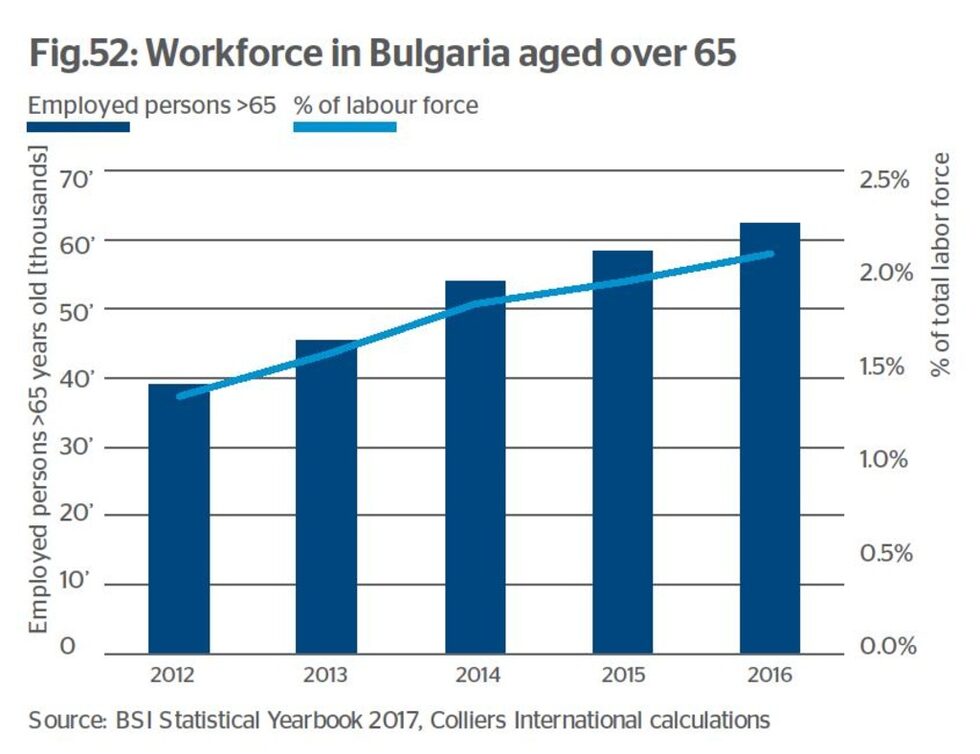

In Bulgaria, though, the economically-active population is spreading beyond this age range, upwards. Whether due to economic reasons (lack of pension savings, poverty?) or personal choice, more and more Bulgarian workers are not "downing tools" at retirement age. The statutory retirement ages are 61 for women and 64 for men, both of which are being phased up to 65.

At the end 2016, workers over 65 years of age comprised 2.1% of the total labour force and while this figure cannot continue to grow at the rate it has in the last 5 years indefinitely, an increment of 5,000 workers per annum for the next 11 years to 2027 could be modelled. We thus would add 5,000 people per annum effectively to the employed workers total as these people would not be retiring.

![Fig.12: Total, male and female % of workforce with a tertiary level of education in Bulgaria [2000-2016]](https://kinsights.capital.bg/shimg/zx980_4149410.jpg "Fig.12: Total, male and female % of workforce with a tertiary level of education in Bulgaria [2000-2016]")

Unemployment reduction increasing employment

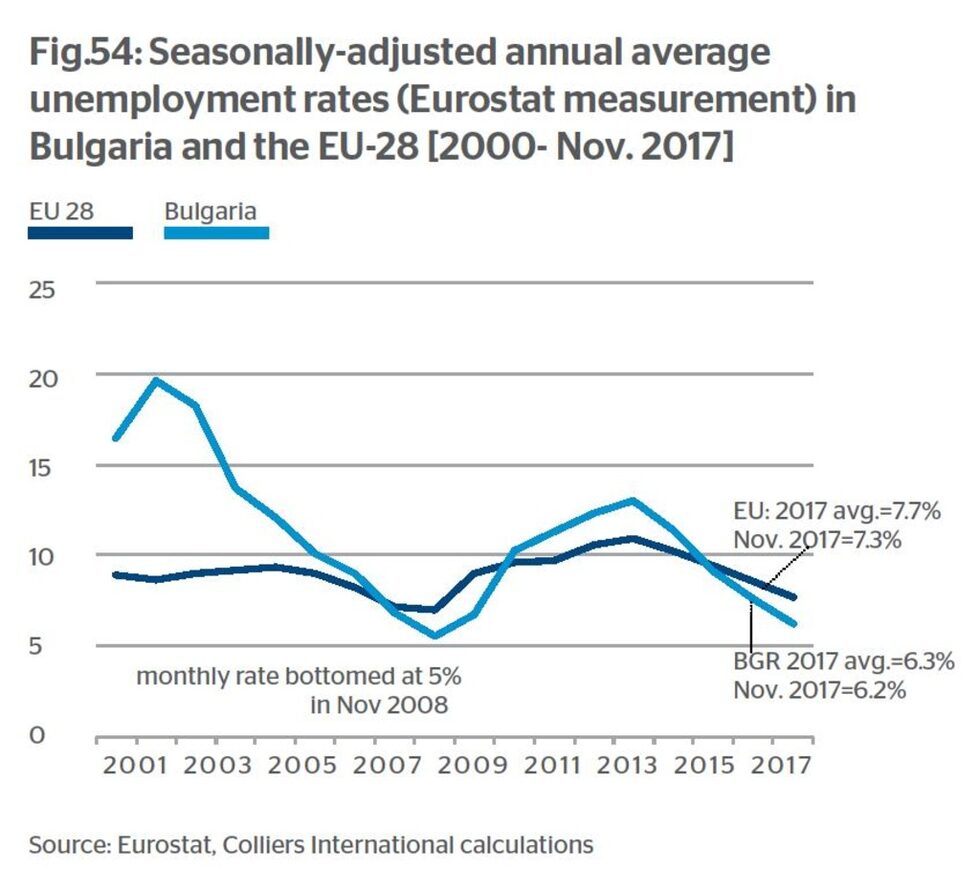

The employed labour force between the ages of 15-64 totalled 2.96 million people at the end of 2016, with another 62.5 thousand employed who were above the age of 65. There were 247.2 thousand unemployed at the end of 2016 according to the NSI and 261 thousand according to the BNB. This latter measure fell to 232 thousand by December 2017, reducing the nationally- calculated unemployment rate from 8.0% at the end of 2016 to 7.1% at the end of 2017. The latter appears to be below the EU average, with Bulgaria's Eurostat-methodology unemployment rate standing at 6.2% in November 2017, below the EU-28's 7.3%.

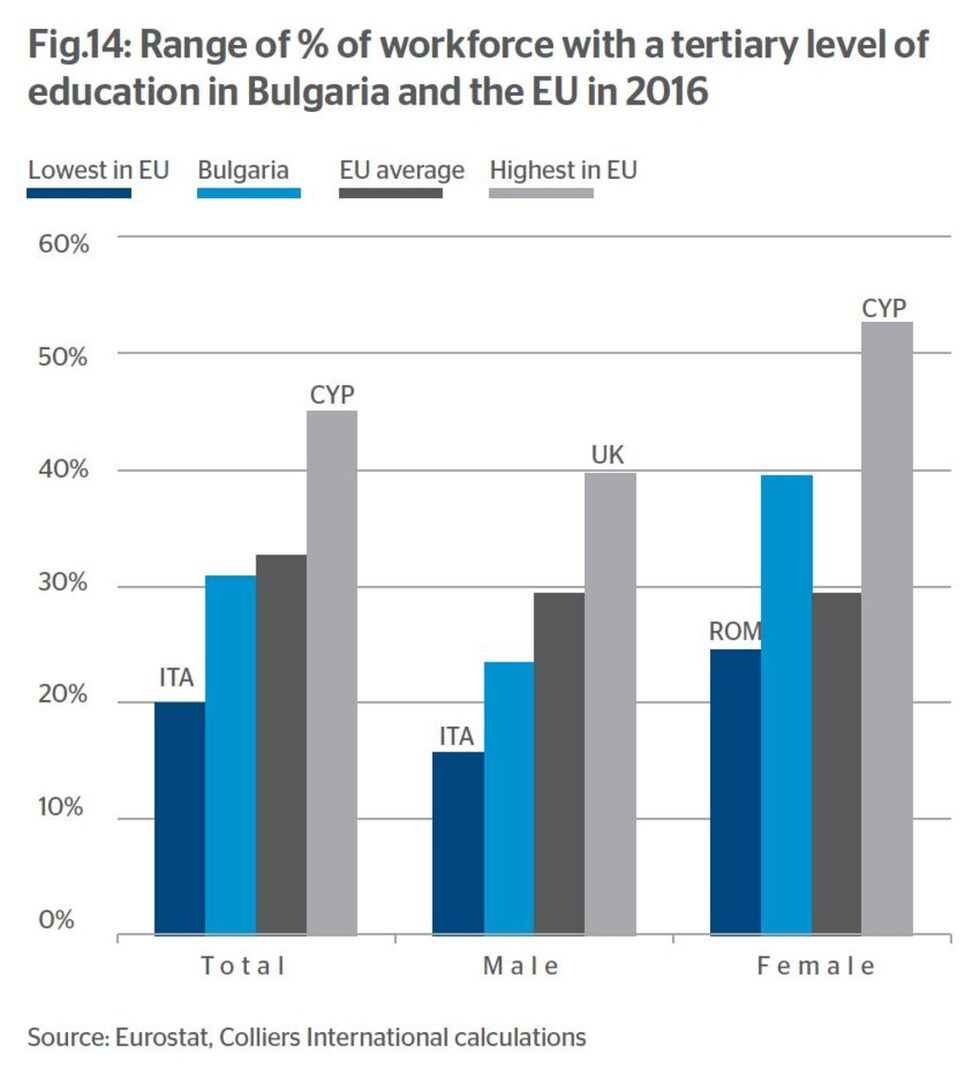

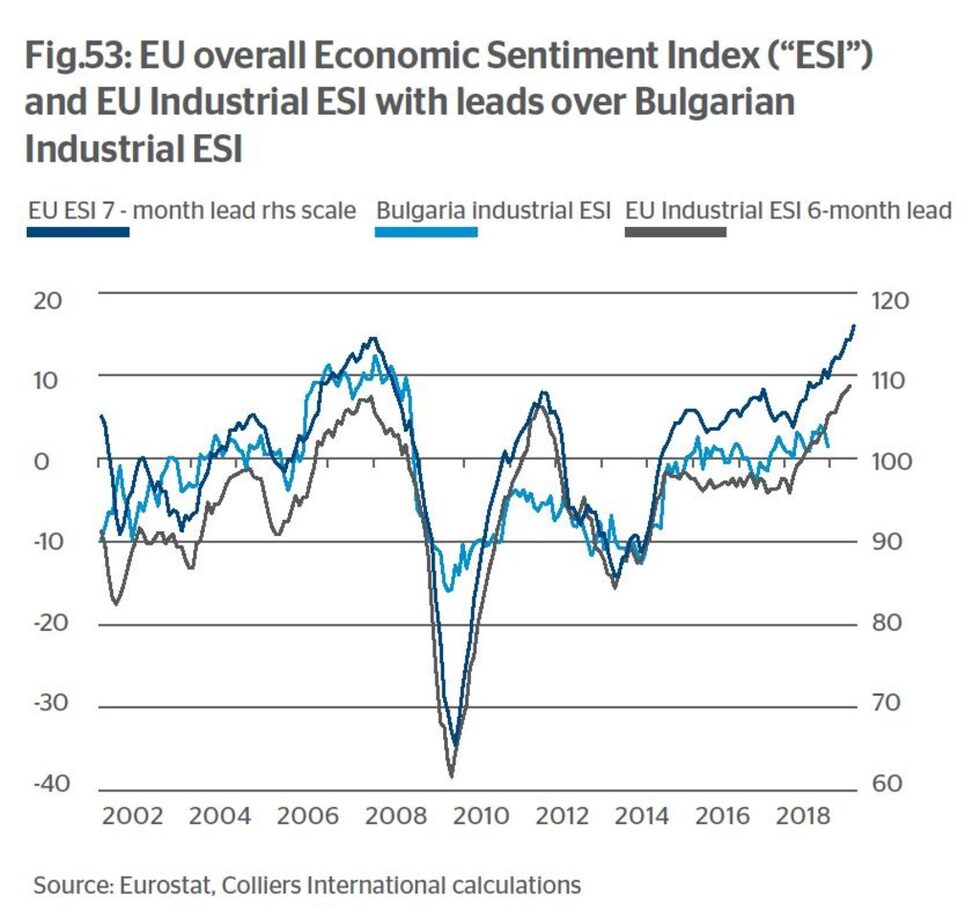

How low can the unemployment rate go through the next economic cycle(s)? Bulgaria's improving proportion of the labour force with tertiary education (noted on Figure 12) and the country's competitive wage cost position in the EU context (see Figure 26) and the buoyancy of shorter run leading economic indicators such as the EU ESI economic sentiment all suggest continued cyclical demand for Bulgaria's exports, production and labour over the next 1-3 years.

This is just assessing the short term. As the economic cycle matures and into the longer run, the unemployment rate should fall and bottom out at around what is classically termed the "non-accelerating inflation rate of unemployment" or "NAIRU" (an economic analysis known widely as the "Philips Curve"). Below that unemployment rate, inflation should pick up as a result of rampant wage inflation due to labour shortages.

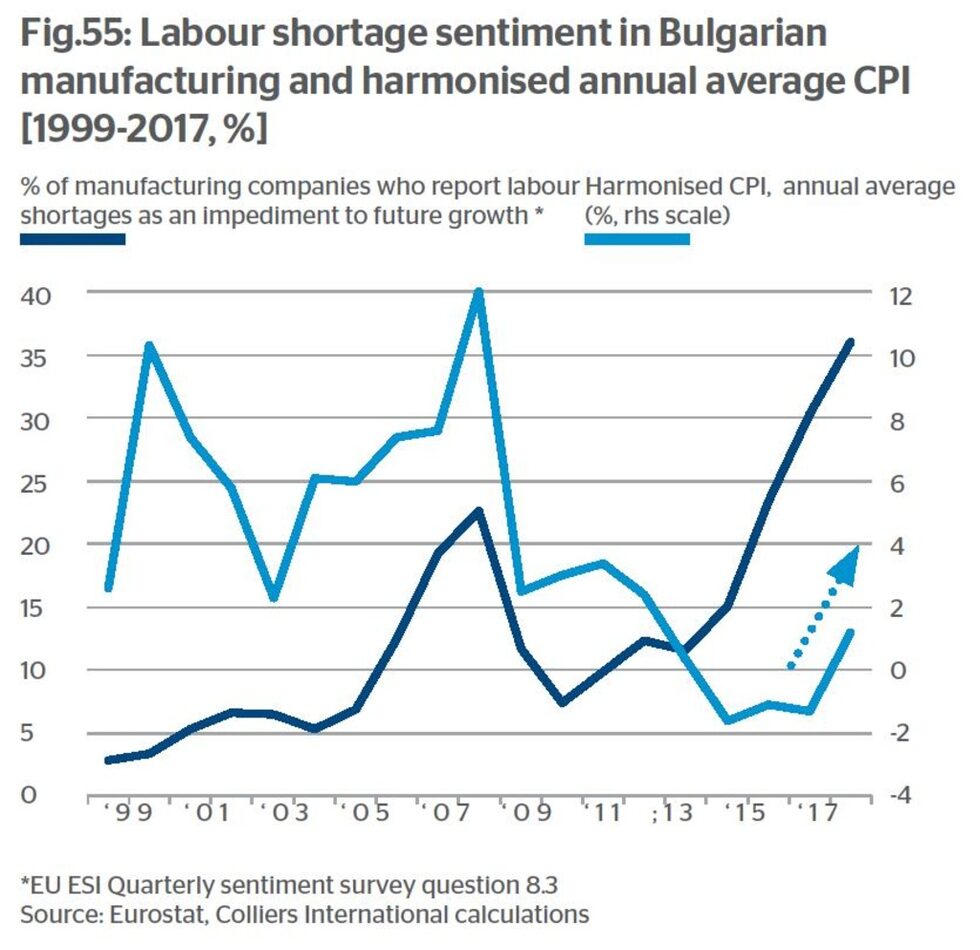

In the last cycle, the unemployment rate in Bulgaria bottomed out at 5.0%. So, there appears to be scope for a further c.1.2% of the labour force to be employed without triggering substantial inflation. 1.2% of the labour force equates to 38,400 workers, or 45,200 workers by the end of 2027 (assuming a larger activity base, see below). Bulgaria's "NAIRU" might well be lower than the previous cycle, as in common with many peers around the world. CPI in this economic cycle has remained subdued, in the range of -2% to 3%. Bulgaria's latest inflation reading came in at 2.1% year-on-year for December 2017. Inflation might well accelerate due to labour shortages as the employment situation tightens: certainly the quarterly sentiment survey of manufacturing companies conducted in Bulgaria and recorded by Eurostat as reporting a full 39% of companies with such shortages providing an impediment to further growth. In all, 38,400 cyclical "spare capacity" in this (and future) economic cycles is not that much.

Potential rise in activity rate increasing employment

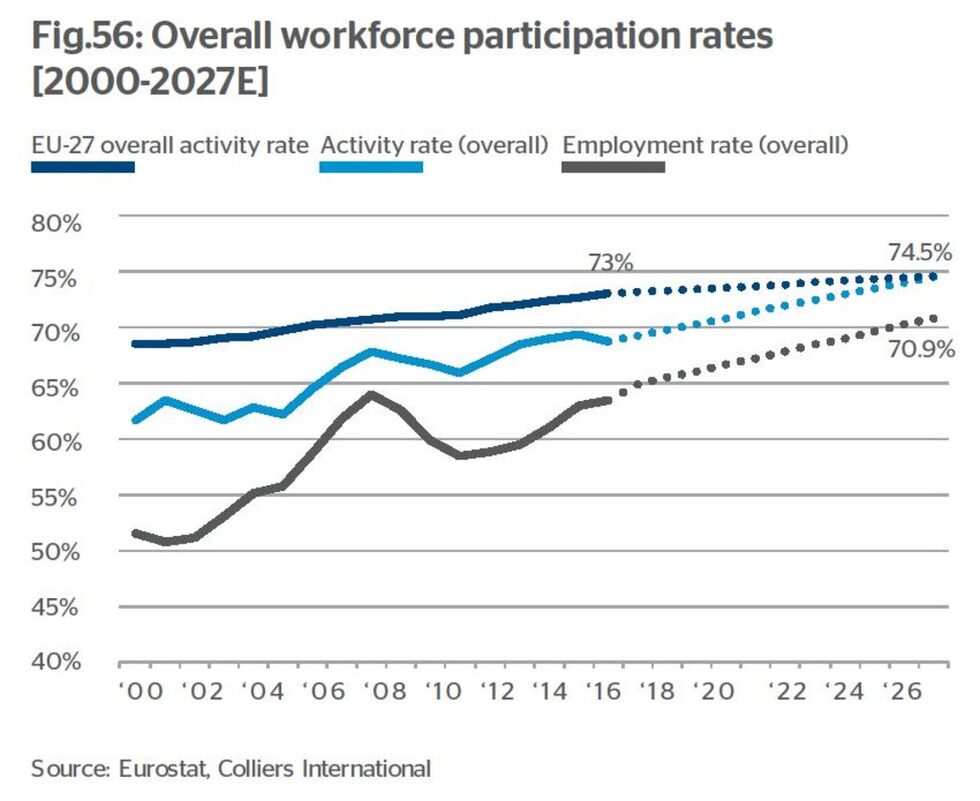

Bulgaria's impressive historical improvement in the activity rate (Figures 23 and 56) from 61.6% in 2000 to 68.7% in 2016 saw it converge towards average EU levels, which stood at 73.0% in the latter year. The high stand-outs within the EU are Sweden, at 82.4% in 2016 and Denmark, at 80.0%. Given Bulgaria's successful push to increase the tertiary education mix within its workforce (Figures 12 and 14), higher skill levels in the workplace through training, higher wage growth in Bulgaria encouraging the marginal worker into the labour force, government efforts to find and train adults not in the labour force, EU funds helping the development of poorly-connected regions and continued rural-urban migration tendencies, we believe the activity rate stands a good chance of converging with the EU average with a 10-year perspective. The activity rate in the EU advanced by 4.5 percentage points over the past 17 years. To assume a halving of this rate of increase would take the EU activity rate to 74.5% by 2027. The corresponding increase in the employment rate would be to 69.8%. With the current size of the 15-64 year-old population of 4.66mn, a step-up of 6.4 percentage points from 63.4% to 69.8% would add 297,800 workers to the Bulgarian labour force in 10 years' time at the end of 2027 (including 2017's employment gains).

Standing in 2027, summing 55,000 workers over the age of 64, 45,200 from a reduction in unemployment to the 5% "NAIRU" (modelled in Figure 56 as a further increase in employment rate) and 297,800 from raising the activity rate implies a total of 398,000 jobs created. This is 36,181 wage-earners per annum over the 11 years. And a growth of 13.5% over the period in total employment.

For the purposes of our modelling analysis, we assume a further climb in the activity rate in the economy to 76.0% in 2037, maintaining the "NAIRU" rate of unemployment at 5.0%; The employment rate thus computes at 72.2%. Modelling participation scenarios out this far is an exercise involving much guesswork about work patterns, hours worked, the impact of technology and the nature of the economy in 20 years' time. The impact of the slower gain in these ratios than in the previous years has an effect on Bulgaria's projected demography and economic growth.

Effect of births and deaths on population size

Can Bulgaria reverse or stem the decline in the country's population aged 15-64? The migration balance appears to be the greater unknown in the next decade. Comparing the change in the number of births over the past few decades, the relationship with the size of the population aged 15-64 15 years later is quite strong. We verified whether there was any upward variation in death rates for the under 15s or the 15-64 age groups that might distort this relationship but found none. It seems to hold that one should eventually expect that the flattening out of the number of births in the 65-80,000 range since the trough in 1997 may mean that the precipitative decline in the 15-64 population levels out. But this phenomenon will not come into play in the next 20 years in a big way, given the yearly exit of significant numbers out of this age bracket into retirement. The age cohorts due to retire in the next 20 years (currently aged 44 and upwards) generally have over 90,000 for each year of age, higher than the present birth rates.

Migration and workforce scenarios

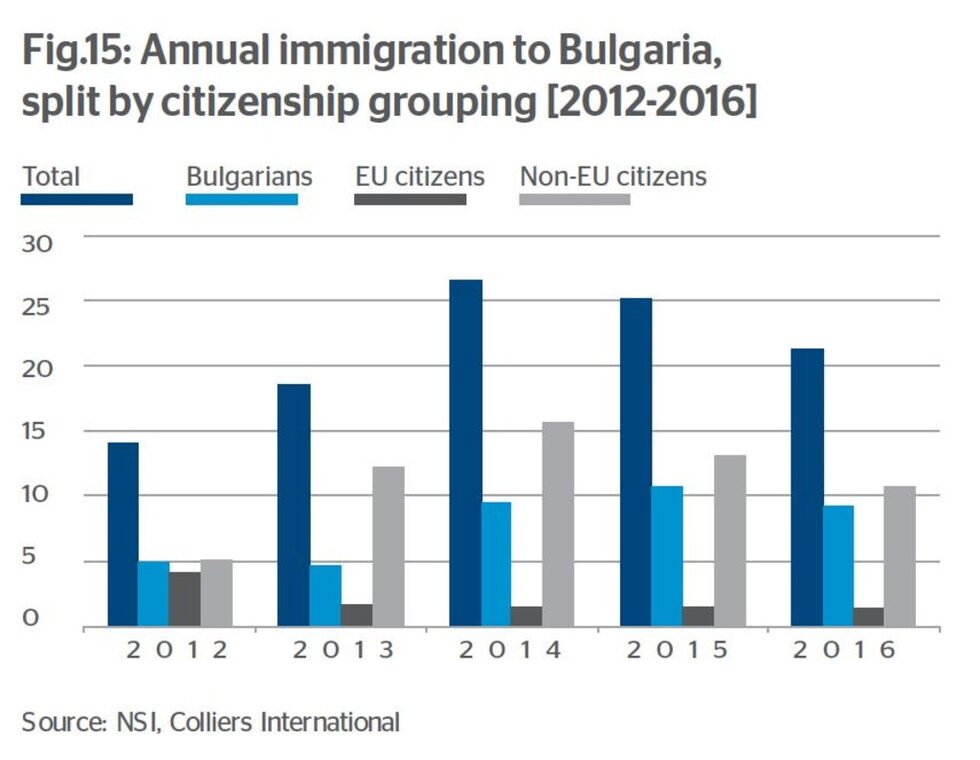

As illustrated on Figure 42 and stated elsewhere in this report, the variation in migration flows has a profound impact on population growth. The historic emigration rate of Bulgarians per annum between 2000 and 2016 using the NSI source was 15,808 and using the OECD arrivals source was 40,778. We adopt these figures as moderate and severe scenarios. We believe other, less malign migration scenarios are possible, including one where immigration balances emigration and one where a more active immigration policy results in an annual influx of 35,000 (or c.0.5% of the population) versus the NSI's emigration estimate of 15,808: a positive immigration balance.

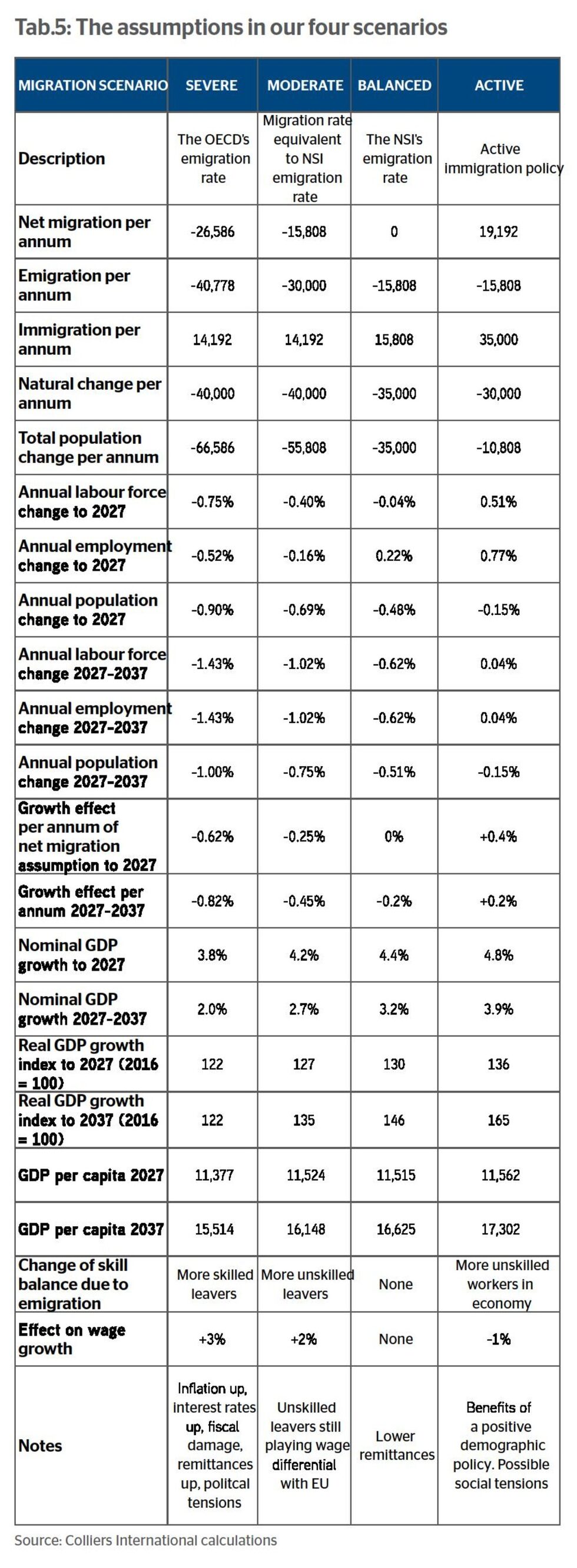

We thus set out four scenarios, balanced migration, moderate emigration, severe emigration and active immigration. We modelled the effect of these four scenarios on Bulgaria's population, working-age population (aged 15-64), economically-active population, or labour force and employed population for the period to 2027 and then to 2037, a 10 and 20 year outlook.

Utilising the evidence from the IMF of the -0.25 percentage point hit to Bulgarian GDP growth between 1999-2014 as a result of the -0.7% per annum population decline seen between 1995-2012 shown on Figures 42 and 43, we estimated the level of adjustment to nominal GDP growth rates due to the net migration balances. We inserted these balances into our forward nominal GDP model and present the resulting variation in nominal and real growth activity.

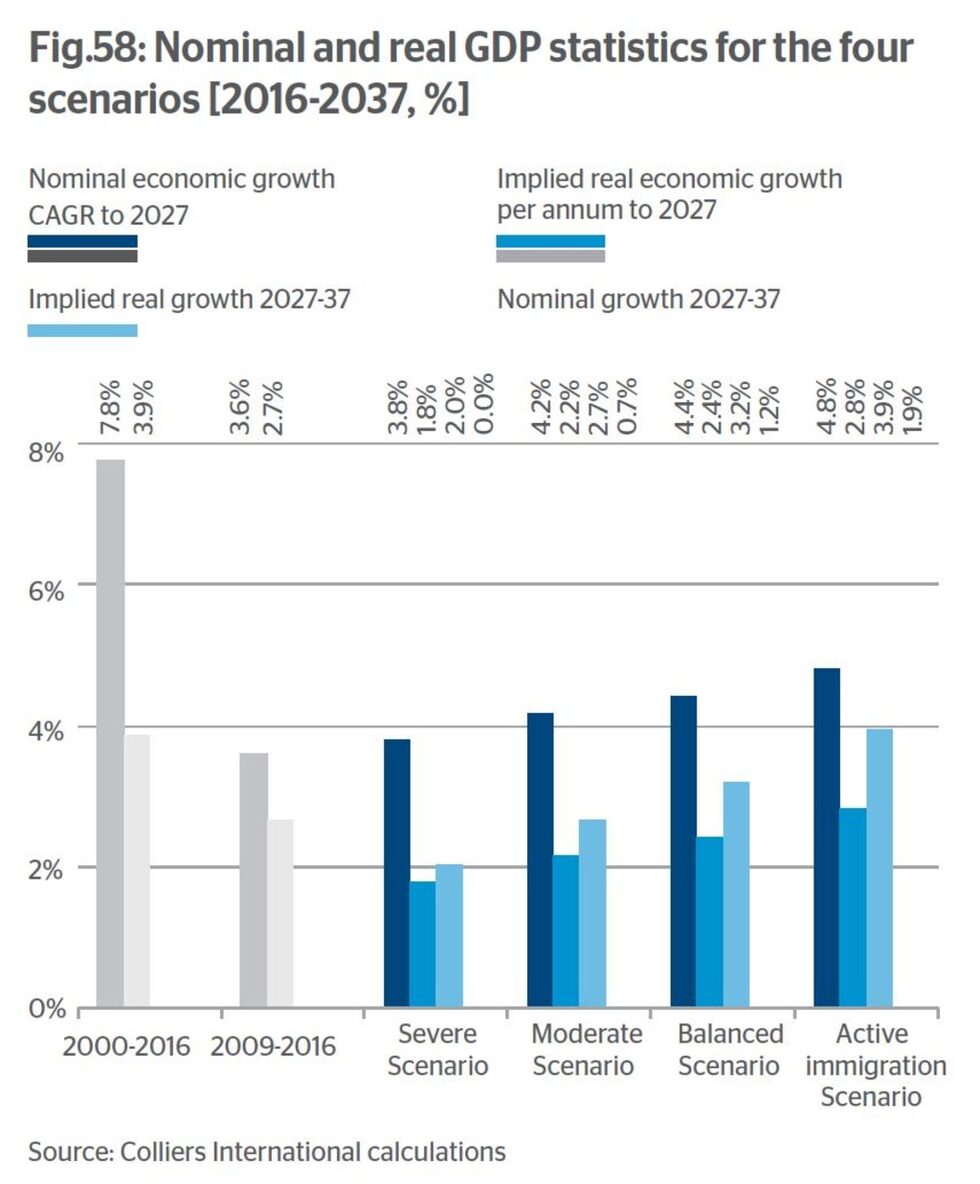

The Balanced Scenario

The cleanest scenario where immigration equals emigration, both modelled at the NSI's 15,808 rate. The balance in the migration picture sees 5,000 more births occur per annum, shifting the natural balance to -35,000. The population shrinks by -0.48% per annum to 2027, edging up to -0.51% in the 2027-37 period. The labour force shrinks marginally to 2027, by -0.04%, as the loss due to the working-age population shrinking is almost matched by the gains in the activity rate set out on Figure 56 and the "bonus" of 5,000 extra workers over 64 per annum up to 2027. For the period 2027-37, no extra over 64s are added and the activity rate "tapers" to 76%, from 74.5%. This tapering reduces the rate of growth of the employment rate, meaning that the labour force actually shrinks by -0.62% per annum.

This differential knocks -0.2 percentage points off nominal GDP growth per annum in all of the scenarios for the 2027-37 period. We see Bulgaria's nominal GDP expanding by 4.4% per annum to 2027 in this scenario, healthy real growth of 2.4%, with CPI fixed at 2.0%. Nominal GDP expands by 3.2% per annum between 2027-37. The economy is 120% bigger than in 2016 in 2037 in nominal terms but has expanded 46% in real terms. The migration balance helps the IT sector drive the GDP growth. GDP per capita rises to EUR 11,515 in 2027 and EUR 16,625 in 2037.

In this scenario of zero net migration, remittances will be lower than in other scenarios.

The Moderate Scenario

The moderate scenario sees the NSI's -15,808 emigration level adopted as the net migration rate. The number of emigrants at 30,000, falls somewhere in between the balanced and severe scenarios. The population shrinks by -0.69% per annum or 55,808 to 2027, edging up to -0.75% in the 2027-37 period. The labour force shrinks marginally to 2027, by -0.4% despite the gains in the activity rate and over-64s working. The labour force shrinks by -1.02% per annum due to the "tapering" of the activity rate between 2027 and 2037.

The IMF's -0.25 percentage point growth scenario is applied up to 2027, rising to -0.45% for the last decade. Nominal GDP grows by 4.2%, real GDP by 2.2% to 2027 and 2.7% nominal thereafter. Real GDP growth then of 0.7% is disappointing but losing -15,808 citizens abroad per annum takes a toll. GDP per capita falls by EUR 477 in 2037 compared to the Balanced scenario. The mix of emigrants is skewed towards unskilled workers, who seek to take advantage of Bulgaria's still cheaper wage profile in the OECD region. The effect of them leaving is a structural squeeze on wages, 2 percentage points compared to the Balanced scenario.

The Severe Scenario

The moderate scenario sees the OECD's -40,778 emigration wave adopted with inward migration falling short and implying net emigration of -26,586. The size of this exodus implies a loss of skilled as well as unskilled workers, much the same pattern as in the last decade. The population shrinks by -0.9% per annum or 66,586 to 2027 rising to -1.0% in the 2027-37 period. The labour force takes a hit to 2027, by -0.75% despite the gains in the activity rate and over-64s working. The labour force shrinks by -1.43% per annum due to the "tapering" of the activity rate between 2027 and 2037. These rates are clearly not sustainable.

The growth scenario is an effect of -0.62 percentage points per annum applied up to 2027, rising to -0.45% for the last decade. Acute skill shortages and fiscal strain due to falling tax revenues contribute -0.2 percentage points in addition to the migration change of -0.42%. Nominal GDP grows by 3.8%, real GDP by 1.8% to 2027 and 2.0% nominal thereafter. Real GDP growth is therefore zero between 2027 and 2037. GDP per capita comes in EUR 1,111 lower in 2037 compared to the Balanced scenario. Emigrants are taking advantage of Bulgaria's still cheaper wage profile in the OECD region and sending back remittances in ever- greater size. Wages are forced up by 3 percentage points relative to the Balanced scenario due to acute labour shortages. The situation would probably bring on some political tensions.

The Active Immigration scenario

This scenario sees Bulgaria deploy an active immigration policy. Immigration flows averaged 21.1 thousand (see Figure 15) in 2012- 16 and the rise to 35,000 is thus not out of scope. Emigration is still occurring, at the NSI rate, meaning a balance of +19,192 feeds into a total population change of just -10,808. More immigrants present boosts the birth rate, due to a likely influx of women of child-bearing age. The population shrinks by just -0.15% per annum in the whole scenario period. The labour force sees a positive change, growing by 0.51% to 2027 and driving employment growth per annum of 0.79%. Unlike the other scenarios, the employment change just stays positive in the 2027-37 period, with the immigration making up for the "tapering" of the activity rate to 76%.

The positive migration balance adds 0.4 percentage points to nominal economic growth which expands by 4.8% per annum to 2027 in this scenario, healthy real growth of 2.8%, with CPI fixed at 2.0%. Nominal GDP expands by a further 3.9% per annum between 2027-37. The economy is 147% bigger than in 2016 in 2037 in nominal terms but has expanded 65% in real terms. Revitalisation of the cities and service sector demand from the immigrants are growth drivers. GDP per capita rises to 11,562 euro in 2027 and 17,302 euro in 2037, 676 euro more per capita than the Balanced scenario.

Immigration has positive causation and the country appears to benefit economically from the positive demographic policy. As is not uncommon elsewhere, some social tensions may arise due to the addition of 0.5% of the population per annum from abroad over a 20-year period. This would take the immigrant population to 550,000, or 12.5% of Bulgaria's population in 2037 in this scenario.

Effects on sector composition of the economy

Our model of the economy assumes fast trend nominal growth of the IT sector (8% per annum), wholesale & retail (6.5%) and manufacturing (6.0%), including auto parts, electrical & optical components, fabricated metals and chemicals. In high-wage growth scenarios, such as the 2017-19 period, the manufacturing sectors may come under some competitive pressure but peers in other countries are also facing high wage cost inflation as well. The economy is hedged somewhat to high wage growth because of the expansion of consumption, the demand for real estate, the increase use of financial products and general services that is a function of high wage growth relative to inflation levels. The IT sector is seen as a growth node, with Bulgaria's intense wage competitiveness in a European context meaning that the level of clustering of expertise will probably be built up fast over the coming economic cycle.

Immigration policy will affect the supply of basic services (availability of cheap labour for routine tasks) and knowledge and talent procurement in the IT sector. The imperative to retain young workers in global-scope industries inside the country will render sectors such as IT and support services somewhat vulnerable to perceptions of the socio-political situation. In terms of probability, we see the "Balanced" scenario as most likely over the whole of the 2017-2037 survey period. Bulgaria's GDP per capita rise in all scenarios suggests that the economic pressure triggering emigration will abate over time, if those GDP per capita levels are rising faster relative to the EU. That "convergence" of GDP per capita is the focus of investment via EU Funds; the focus is not necessarily the population base on which it is based. Crucial in Bulgaria's development is the continued increase in the activity rate, which makes up for the declining natural change input into the 15-64 age population group. Bulgaria has an opportunity to adopt the "Active" increase migration from neighbouring countries and from Russia and the CIS if it chooses to. We believe that on the longer term horizon, many of the social and economic factors pointing emigrants out of the country will abate and a "Labour Force Boomerang" may commence. This is more likely in the shorter run in the Visegrad countries in the CEE due to their higher GDP per capita levels but as time goes by Bulgaria continues to converge with EU norms and measures if there is no political disruption.

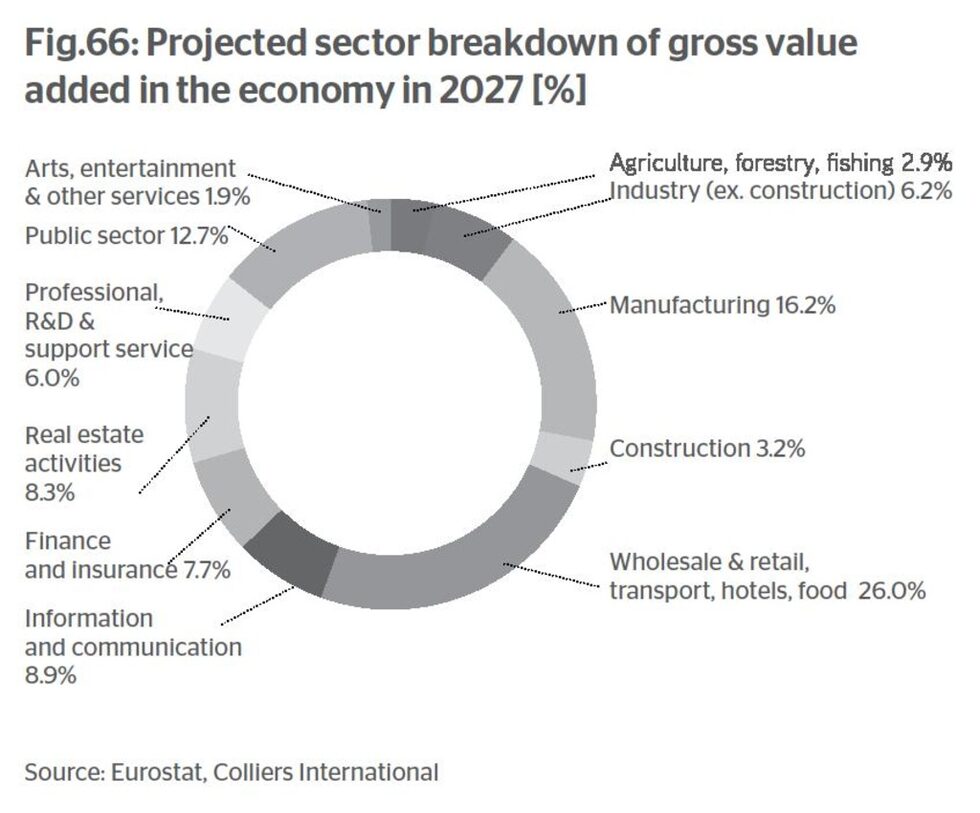

Both the NSI and Eurostat modelled the level of the Bulgarian population out to 2070 and 2080 in studies carried out in 2013- 14. From the 2015 baseline, the NSI saw the Bulgarian population reaching 6.17mn in 2040 in their "target" scenario. Eurostat's baseline scenario for the same date was 5.93mn. Eurostat produced various scenarios as part of their "Europop 2013" project, including one of "no migration". Their population total in 2040 in this scenario was 6.20mn, marginally lower than the Colliers International 2037 total of 6.37mn for the "Balanced" scenario.

Two labour components will affect the size of Bulgaria's economy and its growth rate on a 5-20 year horizon, the first is the number of employed workers in the labour force and the second is the productivity and contribution of that labour force including its total spending in the arena of consumption and services.

Assessing the first component, three factors from a demographic perspective can affect the number of employed workers in the labour force: 1) unemployment rates (a cyclical factor?), 2) the activity rate of the population (the economically-active population versus that total which could be economically-active) and 3) the total population that could be economically active.