- A strong fiscal position, domestic consumption and infrastructure investments will counter some of the effects of the slowdown

Over the past year, economic tensions among the major global economies have intensified, which has led to a considerable decline in economic activity. The increased uncertainty has taken its toll on global investment, manufacturing and trade. Consequently, the modest rebound in global GDP growth in the first half of 2019 appears to have been short-lived, and the near-term outlook has turned notably cooler than expected in the spring. However, both monetary and fiscal stimuli in a number of major economies, including the US and China, as well as resilient labour markets and accommodative financing conditions in advanced economies, are expected to limit the depth of the global slowdown.

As the EU is Bulgaria's key trading and investment partner (it accounts for close to 70% of Bulgarian export of goods), the deteriorating conditions in major European economies, especially in certain manufacturing sectors, will directly affect companies that are part of complex international value chains in the short term. A potential industrial decline and inevitable restructuring will particularly affect businesses that supply capital and intermediate goods to the producers of cars, machinery and equipment where the importance of leading European industrial economies is even higher.

The share of such companies has grown in the last decade, as the Bulgarian economy went through a deep structural transformation. Manufacturing has gradually shifted away from labour-intensive activities towards products with higher value-added. During the previous expansionary cycle before 2008, the Bulgarian economy was mostly dependent on the constant inflow of foreign capital; since 2009 the key driver of growth is the integration into the production supply chains of the leading EU economies. Similar trends affect services, as IT development and business processes outsourcing experienced a huge expansion in both export value and employment.

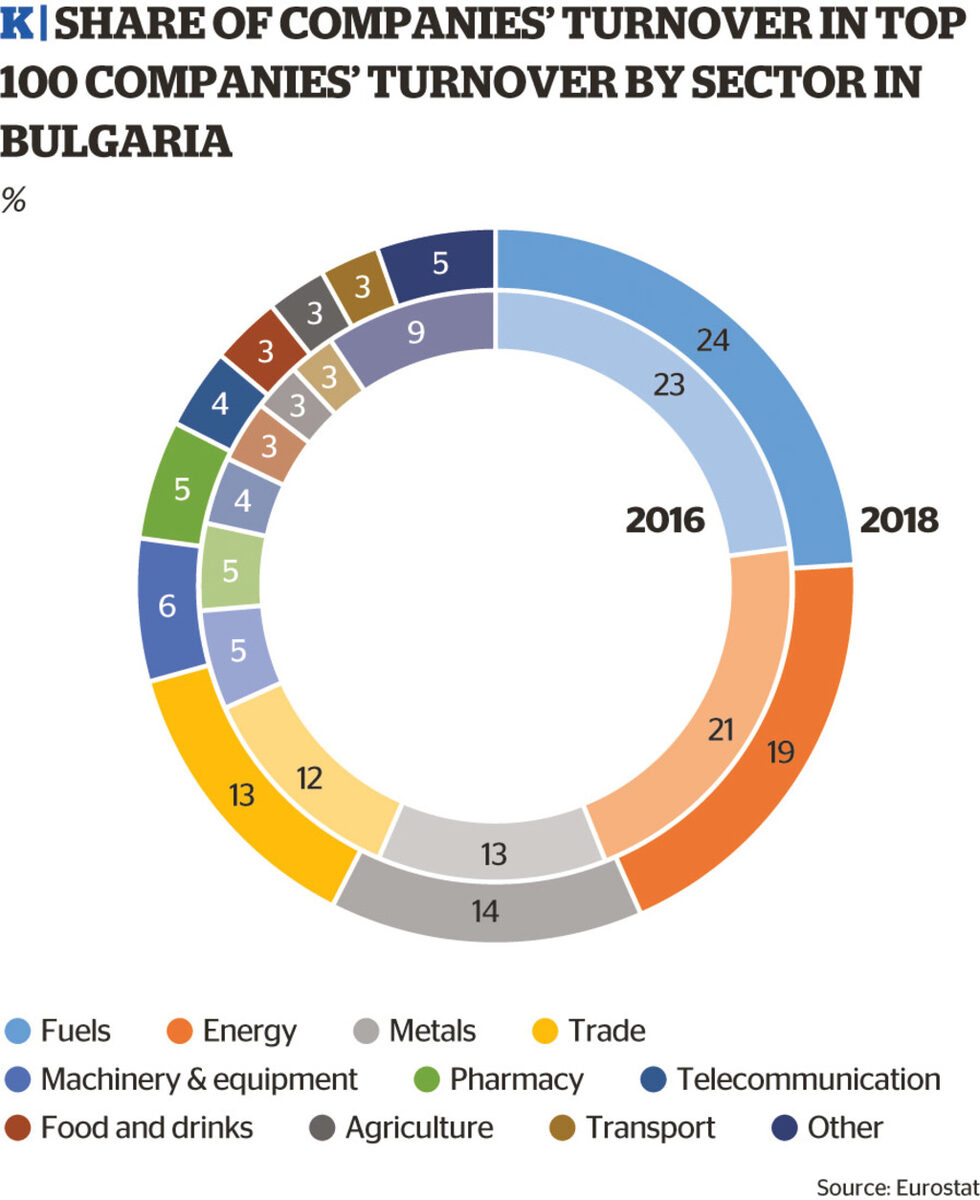

During the period 2016-2018, the ranks of Bulgaria's Top 100 companies were gradually filled with more and more export-oriented firms. For example, the share of turnover of companies in the sectors of energy, telecommunications, and food and drinks in 2016 was around 28% of the turnover of the Top 100 companies in the country, while in 2018 it was 26%. During the same period, the share of turnover of companies in the sectors of metals, machinery, and pharmaceuticals has increased from 22.6% to around 26% in 2018.

In the short term, the deeper integration of Bulgarian businesses into EU manufacturing and business services value chains goes hand in hand with higher exposure to negative developments in the advanced economies, and mostly Germany. From a broader perspective, a prolonged period of stagnant investment and private consumption in the EU will pose challenges to the entire exporting sector in Bulgaria, as demand will be subdued while competition to retain or increase market share will intensify.

As Bulgarian exports to the United Kingdom are rather modest, the potential negative effects from Brexit will affect Bulgaria through the overall deterioration of manufacturing sales to the UK in a scenario of an unfavourable trade deal post-2021.

Nevertheless, the Bulgarian economy has its strengths and comparative advantages, which may counter some of the effects of the euro area slowdown. A sound fiscal position and resilient economic growth - without a build-up of sizable macroeconomic imbalances, are notable in comparison to the indebtedness and anaemic growth in most of the euro area. The performance of the heavy industry, especially in processing fuels and metals, the transformation of manufacturing (gaining a higher share of CEE exports into the leading EU markets), and the positive development of ICT (being the most dynamic sector in recent years), will be crucial for shaping the Bulgarian economy in the near future. These are also the key features of a positive scenario for steady economic convergence even if the EU enters a prolonged period of stagnant new investment and industrial slowdown.

Early signs of pains

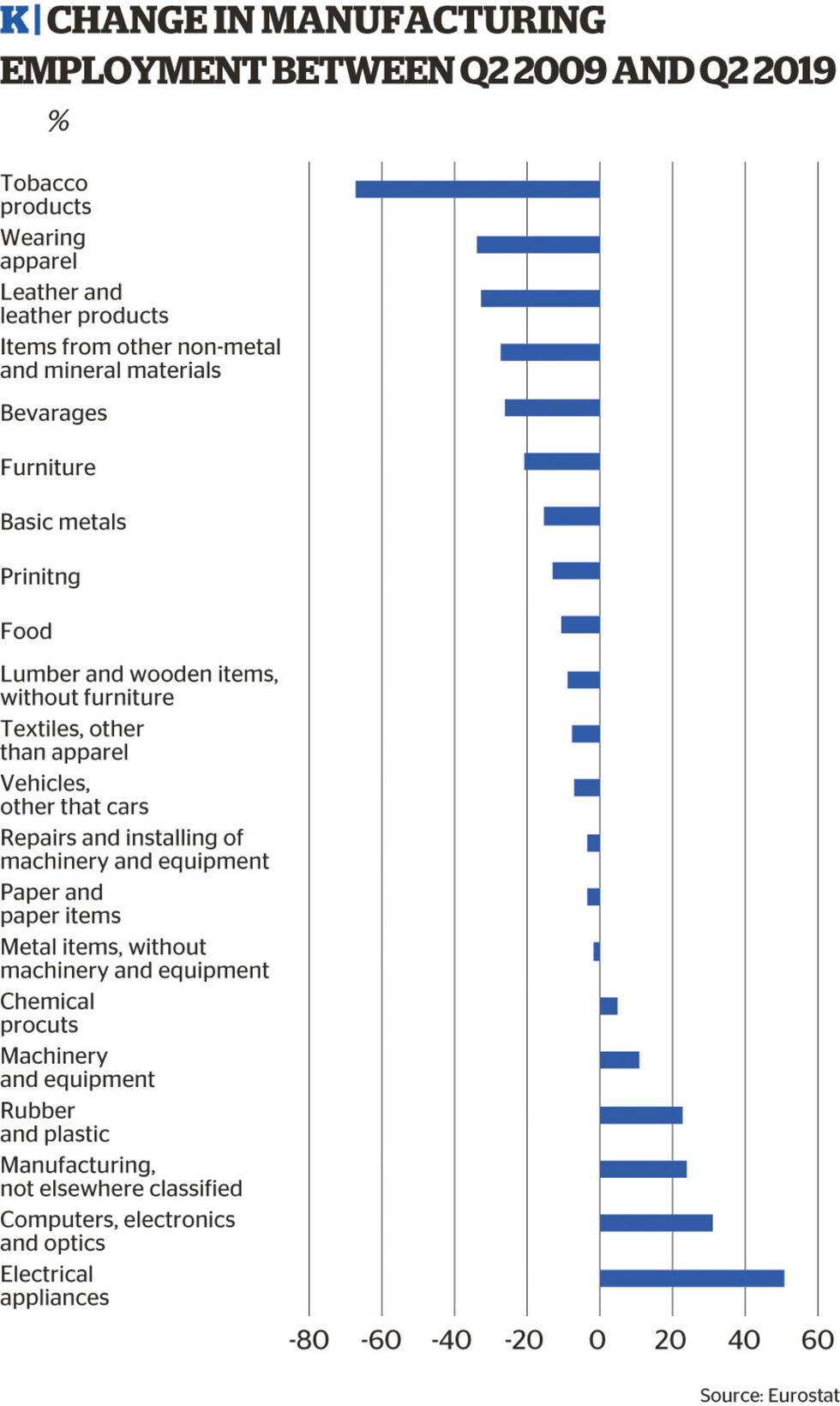

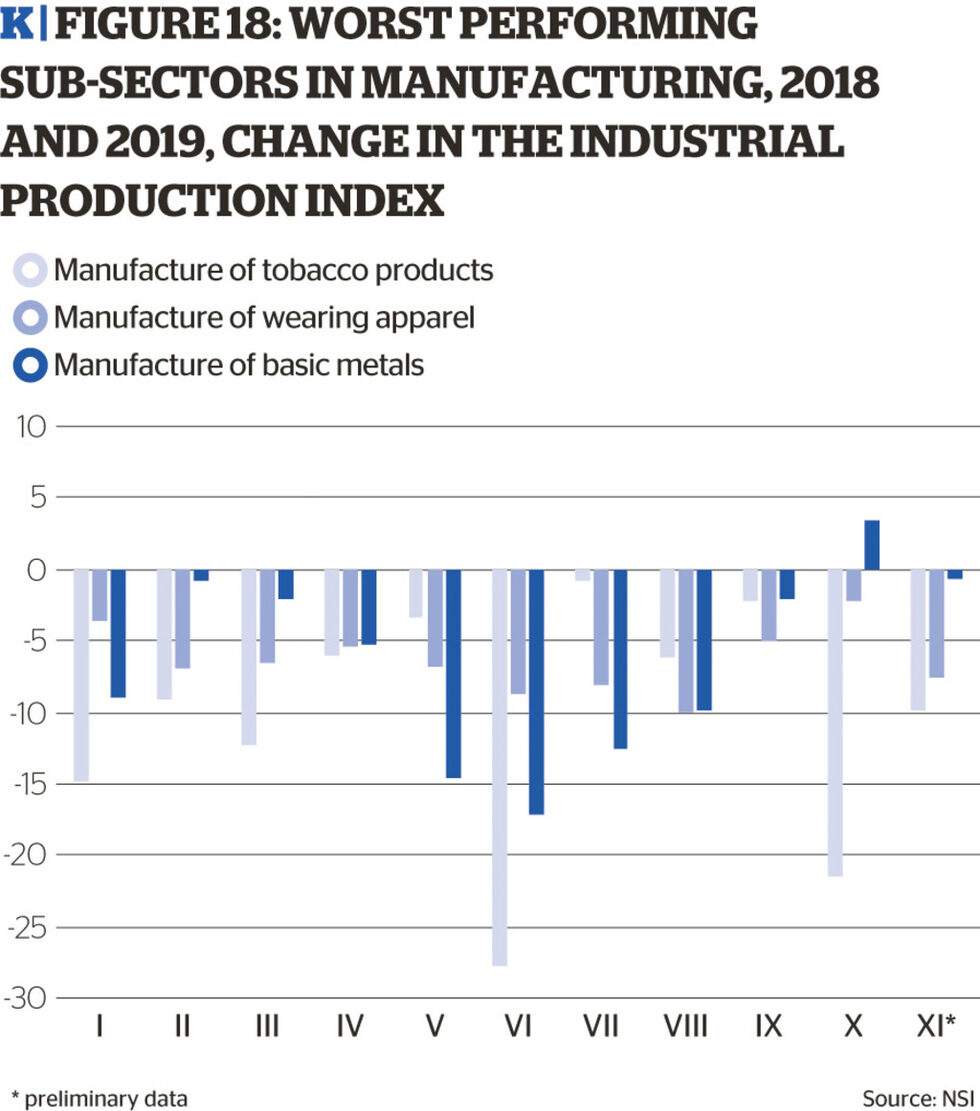

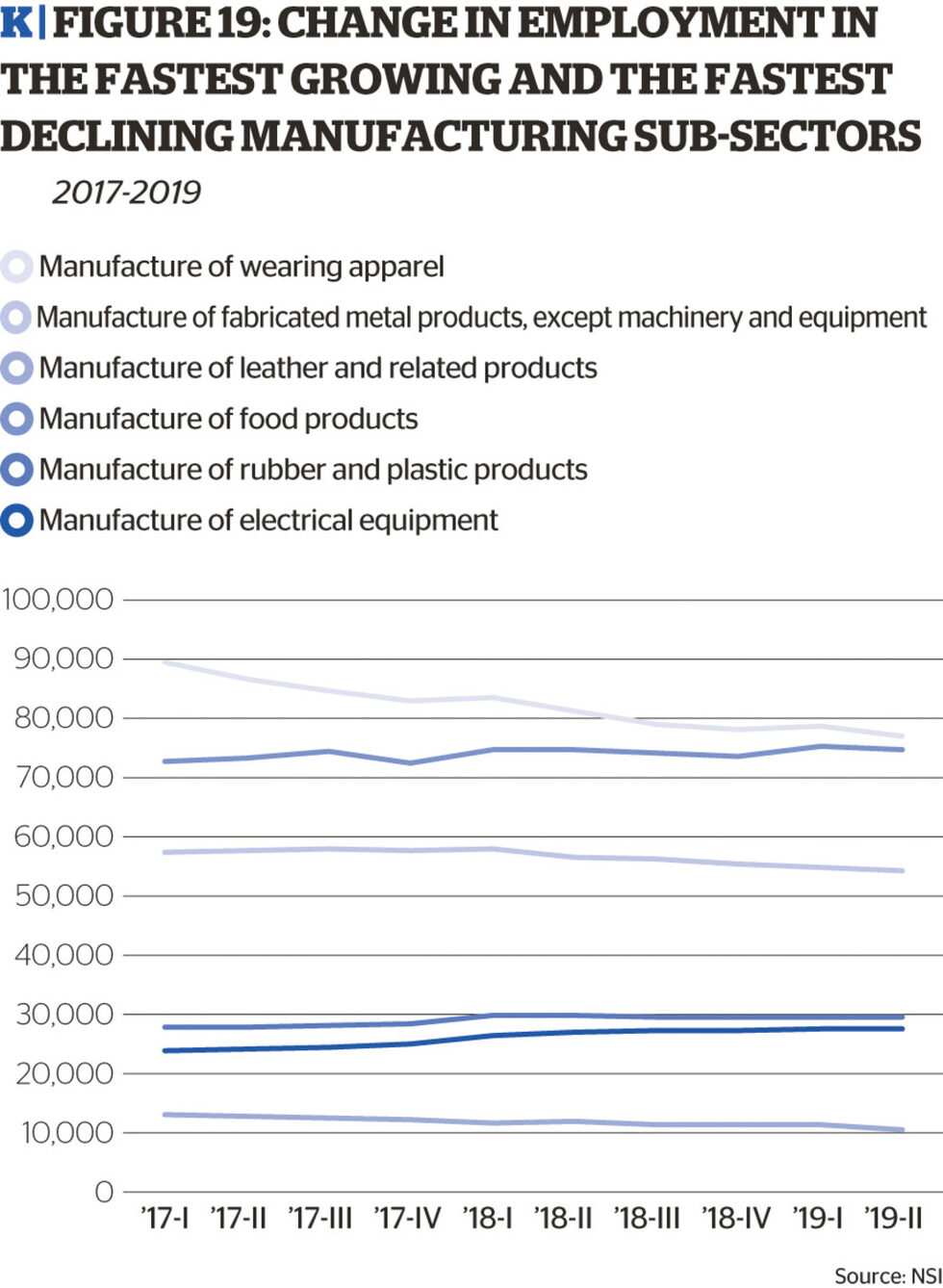

Bulgaria is already feeling the effects of the synchronized global slowdown (a term coined at the IMF). The latest 2019 data suggests that some industries are already losing steam - the decline in basic metals production, particularly during the summer, shows some exposure to the global slowdown.

For most manufacturing sectors 2019 production volumes remain similar to those of 2018. Exports from Bulgaria also remain for the most part stable, especially within the EU despite negative developments in German and Italian manufacturing export industries throughout most of last year. Only two manufacturing sectors (sports goods and transport equipment) saw a 30-50 percentage points increase in sales, while the rest were, at best, stagnating.

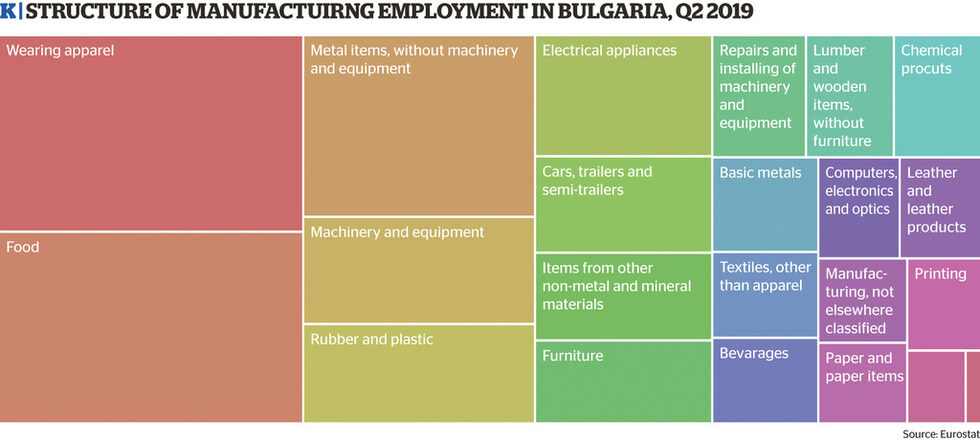

Employment data also shows early signs of stagnation. The most interesting trend is the decline in employment in the manufacture of fabricated metal products, despite stable productions rates. On the one hand, this very well may be a consequence of investments in capital that lead to increased productivity. On the other hand, it is also possible that businesses are expecting a slowdown and lower demand for their product, reducing their labour force in advance. At the same time, in the second quarter of 2019, the output of rubber and plastic products and electrical equipment (both related to the automotive sector, among others) are approaching 30 000 employees each, with little sign of a slowdown in expansion.

Only two sectors - apparel production and manufacturing of leather products, have been rapidly losing workers (the former is down by more than 10 000 in less than two years), but this has to do more with the increase of labour costs in Bulgaria rather than with the global slowdown.

Automotive, electrical equipment and machinery production

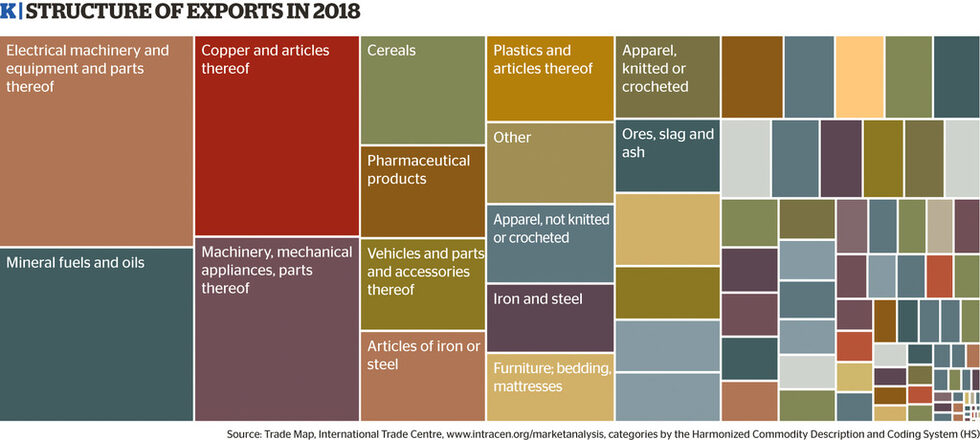

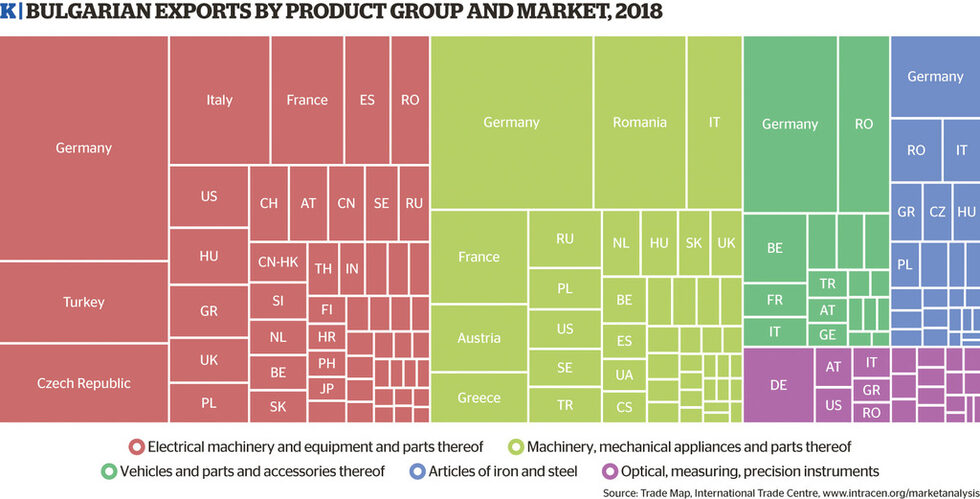

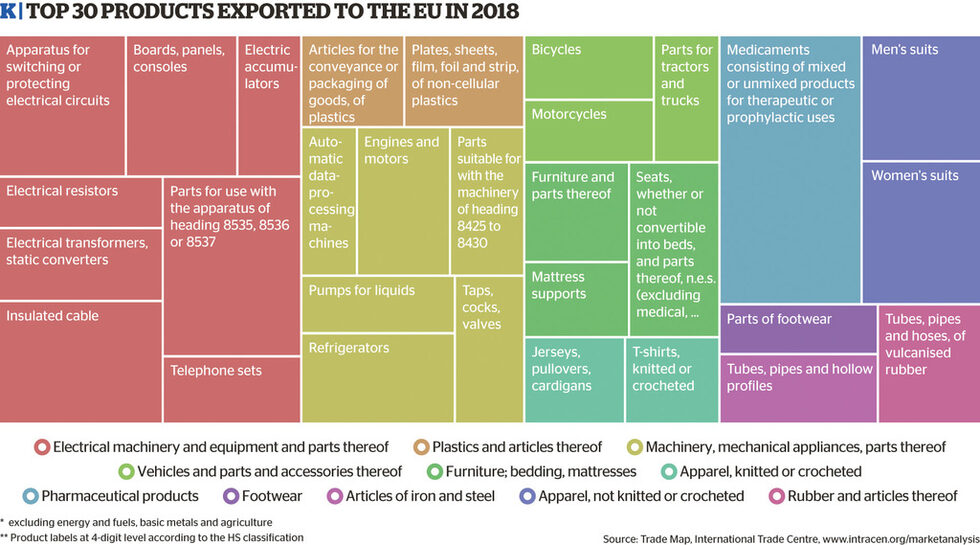

Three sectors will be most likely affected in a negative scenario of a global and EU manufacturing downturn - automotive parts, electrical equipment and machinery which represent 23.4% of Bulgarian exports, or about 6.2 billion euro in 2018, and are heavily dependent on external demand. The downside impact on their performance will be relatively strong because they are export-oriented and do not rely on domestic demand. At the same time, they produce predominantly intermediate and investment goods, and as such are deeply integrated into international value chains.

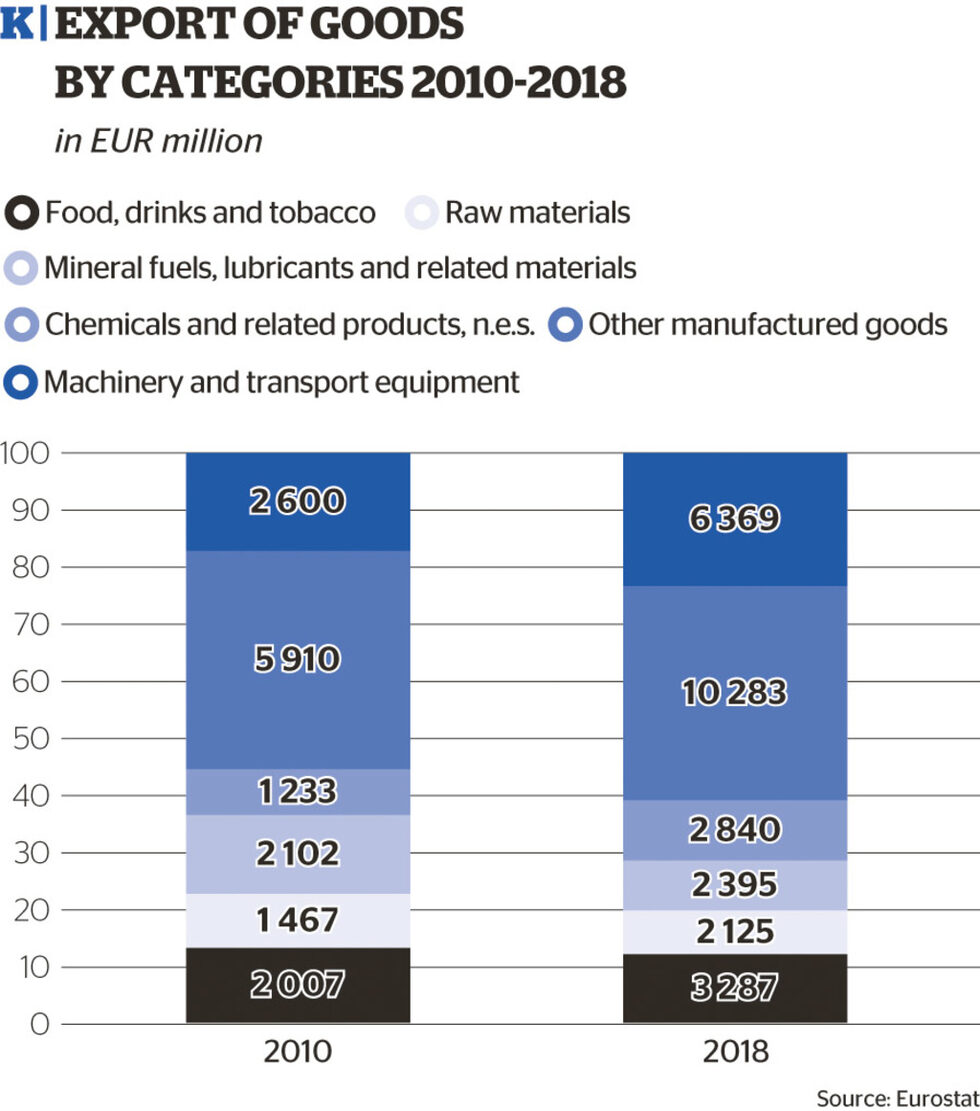

Exports of electrical machinery and equipment reached 3.1 billion euro in 2018 and became Bulgaria's leading group of export products. The growth between 2013 and 2018 was the highest among key export products, reaching 76%. Compared to 2008 - the peak year for Bulgarian exports before the 2009 crisis - exports of electrical machinery and equipment are 3.4 times higher and their share in total exports grew from 5.9% to 11%.

The automotive industry was the second fastest-growing among the big manufacturing sectors in the last decade. Ten years ago it ranked 23rd in Bulgaria's exports with less than 1% of the total value. In 2018 it reached a share of 3.1% after a 65% growth in the period between 2013 and 2018.

Exports of machinery and mechanical appliances were slightly below 2.3 billion euro in 2018 and remained number four product group in Bulgarian exports. They grew by 42% in the last five years; since 2008 the value of those exports doubled. The share of machinery and mechanical appliances in total exports grew modestly - from 7.5% in 2008 to 8.1%.

The prospects of slow growth in the EU will depress new business investment, which particularly affects the demand for capital goods. About 77% of Bulgarian products are exported to the EU market - some 87% in the automotive industry, 80% in the machinery and mechanical appliances and 71% in electrical equipment. EU automotive and machinery production will probably be hit most severely by uncertainties about the rules of international trade and the slowdown in global investment, and particularly investment moderation in China - the two industries accounted for 480 billion euro or 25% of EU exports to the global market.

As these three sectors are rather capital intensive industries, the relative share in manufacturing employment is slightly lower - about 16.5%, or about 82 000 workers in the first half of 2019. It should be noted, however, that these three sectors added more than 20 000 jobs in the last six years despite the long-term process of improving labour productivity through capital investment.

Additionally, two other industries will be relatively strongly affected in this scenario - the manufacture of iron and steel products, and optical and measuring instruments and appliances. They accounted for 2% and 1.4% of Bulgaria's total exports in 2018, respectively, or about one billion euro combined. About 86% of iron and steel products were sold on the EU market, while for the optical and measuring instruments the share was 66%. The two industries employed about 65 000 workers in the first half of 2019 and both have added jobs since 2013.

Germany is the top export destination for all of the five manufacturing product groups. The other key markets are Italy, Romania and the Czech Republic - all major industrial economies in the EU - and Turkey. It should be noted that the share of Germany in all product groups has gradually increased during the last five years.

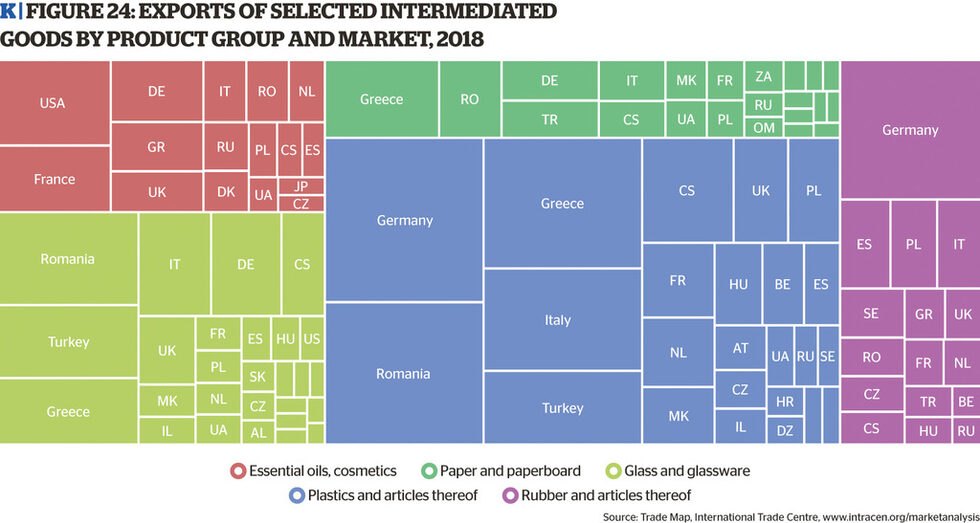

Chemicals, paper, glass and similar products

Manufacturing of chemicals, paper and glass is also highly dependent on global trends. However, they are not that closely integrated to the key industrial economies of the euro area compared to the export-oriented automotive and machinery production. Markets are more diversified, with stronger importance of neighbouring economies, as Romania, Greece, Turkey and Serbia are typically among the major importers. This pattern might alleviate a potential cut in orders from external business partners in case of short-term shocks in global demand, but a medium- to long-term EU-wide manufacturing slowdown will nevertheless affect these industries.

Production of plastics and plastic articles reached 830 million euro in 2018 or about 3% of total Bulgarian exports. The growth since 2008 was comparatively low - about 68%. At the same time, manufacturing of rubber products grew 4 times, reaching 300 million euro in 2018.

Exports of essential oils and cosmetics preparations have also increased substantially - by 3.4 times since 2008. Exports of glass and glassware more than doubled, while exports of paper and paperboard grew 2.3 times. Altogether, the five industries accounted for more than 7.3% of Bulgarian exports in 2018 or about 2.1 billion euro.

Consumer goods

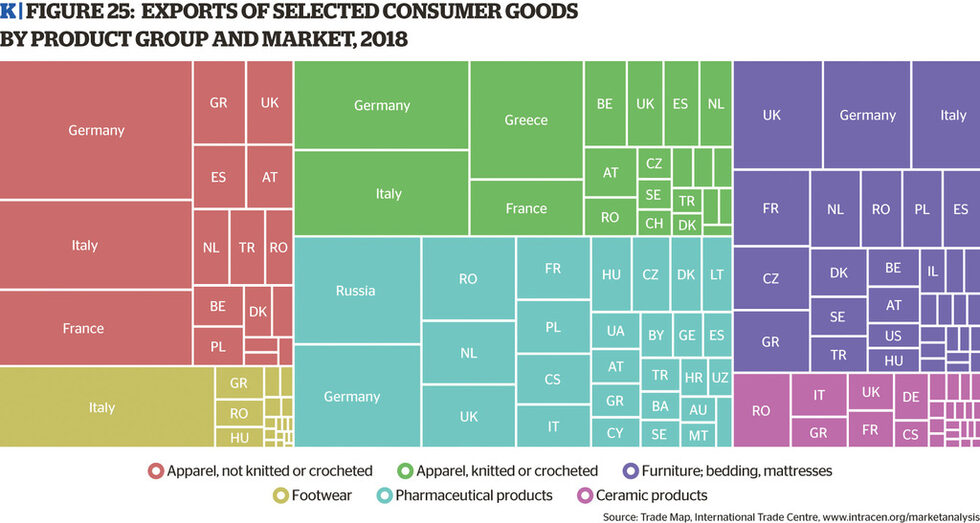

Bulgaria's exports of consumer goods should not be directly affected in the short term by a deterioration of global trade conditions or a slowdown in major EU export sectors such as transport equipment and machinery. A prolonged period of stagnating growth in the EU, however, will subdue demand for products made by Bulgarian suppliers. Several important factors should be considered here.

First, exports of clothing and footgear are on a long-term decline. The major factor is the increasing cost of labour. Competitive pressure is gradually rising and industries are transforming by shifting into products with higher value-added while investing in capital to replace manual labour. Within the apparel industry, exports of knitted clothing grew by 18% since 2008, while exports of not-knitted clothing fell by 5% during the same period. Overall, exports were slightly growing both in the last decade and the five-year period after 2013. However, the growth rate was close to zero and much lower than the average increase in exports. The value of footgear exports increased by 27% since 2008 - well below the average. Statistical data on end-markets is misleading, as some exports that are recorded in Germany or Italy are further distributed to other countries. Still, the overall share of the EU is above 90%.

Pharmaceutical exports are geographically diversified and the share of the EU market in them is slightly below average at about 65%. This is one of the fastest-growing industries with a 3.7 times increase in the value of exports since 2008 and a share of 3.1% in total Bulgarian exports in 2018. Russia and Serbia are key markets.

The sectors of furniture, bedding, mattresses and ceramic products depend on both household spending and business investment. The overall conditions for households in the EU - employment, disposable income, access to credit - will directly affect demand for finished products. At the same time, new investment such as new buildings, hotels and offices will also play a key role in the future market. In any way, a scenario for prolonged slow growth in Europe will put downward pressure on demand for these products, although it is highly unlikely that a huge shock can occur in the short term. Exports of ceramic products doubled since 2008 and accounted for almost 1% of total exports in 2018. Exports of furniture, bedding and mattresses trebled to reach a share of 2.3% in total exports. The final destinations are quite diverse with no country having a dominant position.

Overall, these six industries accounted for more than 3.3 billion euro of exports in 2018, or 11.9% of the total. From a labour market perspective, clothing and footwear manufacturing is downsizing employment as a key strategy for retaining competitiveness. Since 2010 the number of jobs decreased by 73 000; the decline continued even after 2013 with 30 000 lay-offs.

Still, clothing and footgear production account for over 17% of total manufacturing employment. The downsizing - both due to companies moving to cheaper production destinations and replacement of labour by capital - will continue in any scenario for the EU economy. The furniture, bedding and mattresses production is exposed to similar labour cost pressures but the fast growth in exports has prevented a sizable decline in employment in the sector. It is still a relatively important part of the manufacturing jobs market with 19 000 workers. Pharmaceuticals and ceramics are capital-intensive industries and their share in overall employment is low - about 2% or 10 000 workers.

Bulgarian economy's strengths

The foundations of the Bulgarian economy are significantly different in comparison to the previous boom. It ended with the so-called Great Recession that began at the end of 2008. Economic growth in recent years is supported by the transition to more knowledge-intensive activities, with most of them taking advantage of export markets. While the previous expansion cycle was dependent on the constant flow of foreign capital channelled through direct investment or banking credit, the current cycle is characterized by the export-led growth of manufacturing and services and private consumption.

Fiscal policy is quite prudent, with year after year of budget surpluses and government debt is projected to decrease below 20% of GDP in 2022. This favourable fiscal position is extremely important in the face of a euro area slowdown and the buildup of negative expectations throughout the leading EU markets. The recent decision of S&P to increase the credit rating of Bulgaria to "BBB" with a positive outlook is a result of the resilient economic growth of Bulgaria, without building macroeconomic imbalances.

The growth of the Bulgarian economy in 2020-2022 should also be supported by strong domestic demand, as private consumption will continue to be the major driver. Consumer spending is supported by favourable conditions on the labour market - the employment rate in the 20-64-year age group reached 76.3% in the third quarter of 2019, while nominal wages increased on average by 12% in the first nine months of 2019. Loans to households, expected to have increased by 10% in 2019, will further propel private consumption and residential construction. The pace of growth of private consumption is expected to slow down, as future employment growth will be limited, but nevertheless, consumer spending will continue to support domestic demand. Growth of public spending on huge infrastructure projects is also to be expected, mostly in the framework of EU funds.

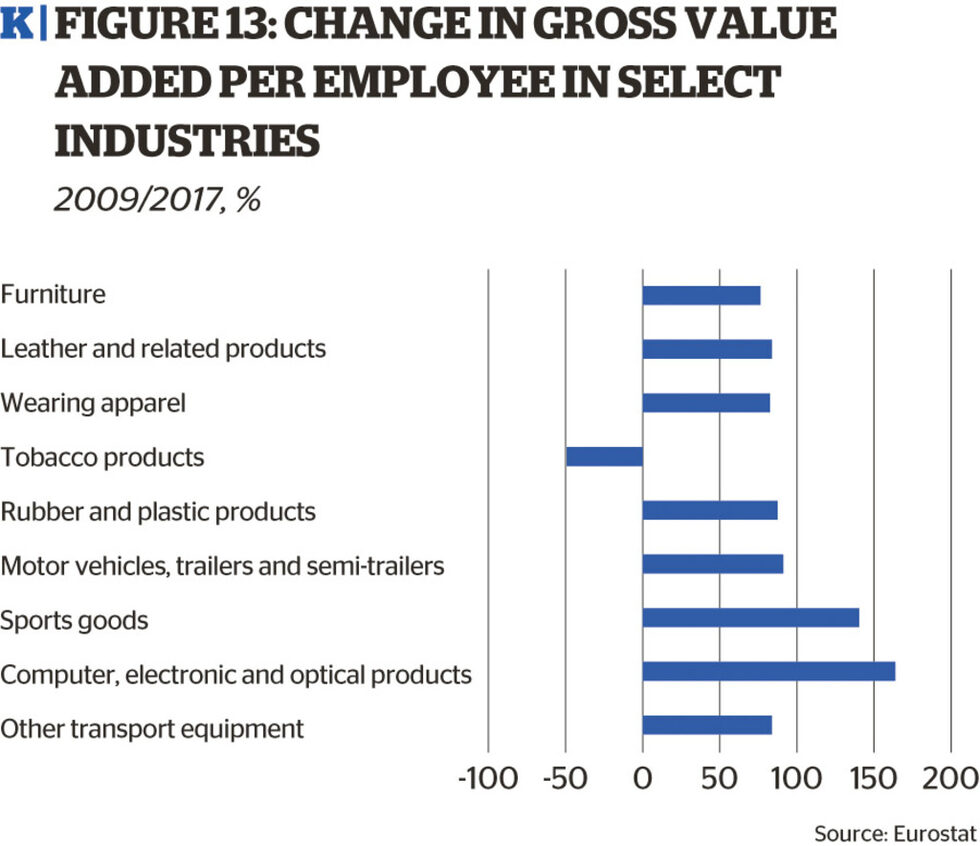

The transition in manufacturing from traditional sectors like apparel or furniture (with the added value of 6-7 thousand euro per employee) to more capital-intensive industries like machinery and equipment, electrical equipment, motor vehicles, computers, electronic and optical products (with the added value of 14-15 thousand euro to 20 thousand euro per employee) will most likely continue even in a scenario of a continuous slowdown in the euro area.

Bulgaria still holds only around 2% of Central and East European (CEE) countries' exports to Germany and Italy in electrical equipment and machinery, but the share is increasing in recent years. CEE countries have a competitive advantage in those sectors and their share in Germany's imports of machinery increased from 18.7% in 2014 to 20% in 2018. Bulgaria follows this trend, increasing its share in CEE exports of machinery to Germany - from 1.6% in 2015 to 1.82% in 2018. A similar dynamic is observed in electric equipment. As Bulgaria will most probably continue to integrate deeper into the EU's largest markets and increase its share in CEE exports (this process intensified in the last two years), those sectors may be in a position to soften the impact of a continuous slowdown in the euro area.

Bulgaria's comparative advantages in those most dynamic sectors are supported by the rush to create industrial parks in the leading economic centres in the country.

As labour costs will continue to increase and the supply of labour will be limited, low-tech industries, which rely on cheap labour, will face additional challenges. In 2019, there were already a few examples of low-tech companies leaving the country and this may continue in 2020. A global slowdown will affect those companies, as they face sluggish demand and increasing labour cost. Some Bulgarian companies in low-tech manufacturing may need to move from the most attractive economic centres to less developed regions of the country. While these processes may create structural problems, they will support the general trend of transformation of Bulgarian industry.

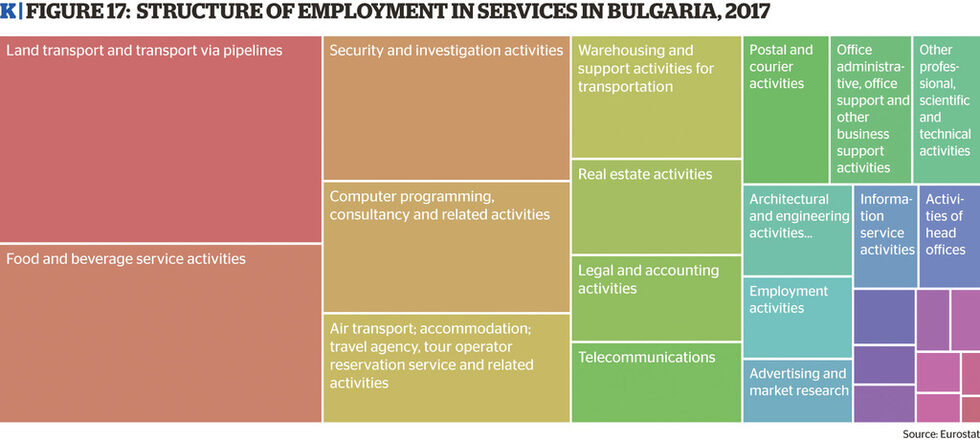

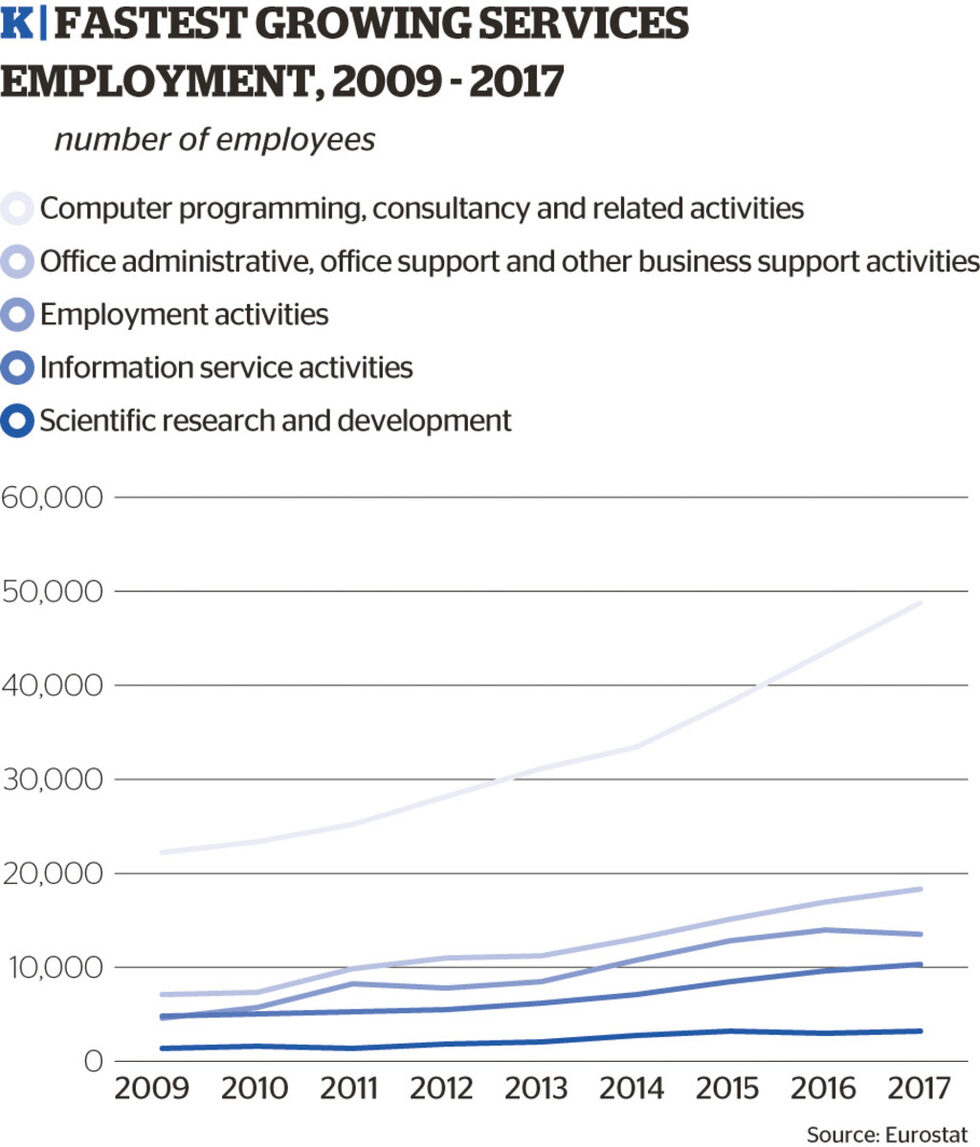

The growth in the ICT sector is likely to continue, as Bulgaria is having competitive advantages, which facilitate more investments in that sector. A global slowdown, even if it affects the financial sector, will not necessarily disrupt the growing ICT industry in Bulgaria. Investment in human capital will be crucial, as labour shortages may be the main constraint to further growth of the ICT business. In that sense, the continuous expansion of ICT in the secondary economic centres (Plovdiv, Varna, Burgas) will also be crucial and should be supported by local communities/authorities.

Much of the growth and expansion of the services sector of Bulgaria in the years following the economic crisis has come from the ICT and business process outsourcing sector. They account for a significant portion of the record labour market expansion in larger cities, Sofia in particular. These activities, however, are also quite distinct in being almost exclusively outward focused, catering to foreign markets.

This, in turn, means that those sectors are not as much dependent on the economic cycles of Bulgaria as they are on the major markets they work for: the UK, USA, Germany and the Netherlands, to name a few of the largest. As a result of this dependency, any major economic downturn in those markets, especially ones triggered by a burst of a bubble in the technological sector, will likely have significant consequences for the Bulgarian ICT and outsourcing sectors even if the country itself is not in a major crisis.

Given the uneven exposure of those sectors to individual markets, it is hard to quantify the exact dimensions of a possible slowdown in the technological field, but it is relatively safe to assume that from 2020 onwards it will not add new employment and expand production at the same rates that it has achieved in the 2015-2019 period. At present, according to estimates by sectoral organizations, outsourcing and ICT services contribute about 5% of the GDP of the country and employ around 200 000 people, thus any risk to its well-being translates into a systemic risk to Bulgaria's economy as a whole, and in particular to its growth potential.

- A strong fiscal position, domestic consumption and infrastructure investments will counter some of the effects of the slowdown

Over the past year, economic tensions among the major global economies have intensified, which has led to a considerable decline in economic activity. The increased uncertainty has taken its toll on global investment, manufacturing and trade. Consequently, the modest rebound in global GDP growth in the first half of 2019 appears to have been short-lived, and the near-term outlook has turned notably cooler than expected in the spring. However, both monetary and fiscal stimuli in a number of major economies, including the US and China, as well as resilient labour markets and accommodative financing conditions in advanced economies, are expected to limit the depth of the global slowdown.