Nearly three years after the dramatic collapse of Corporate Commercial Bank (the fourth biggest bank in Bulgaria in 2014) and the liquidity crisis that threatened the stability of Fibank (the third biggest bank), it can be safely declared that the Bulgarian banking sector has returned to a healthy calm. Bank profits are up, the consolidation of the financial institutions continues, while bank lending rates are steadily converging to the Central European levels.

The real picture is muddled, though. The massive asset quality review and stress testing of the banking sector, carried out by the Bulgarian National Bank in 2016, has shown that even though all of the banks are well capitalized, some of them are, well, in not such a good shape.

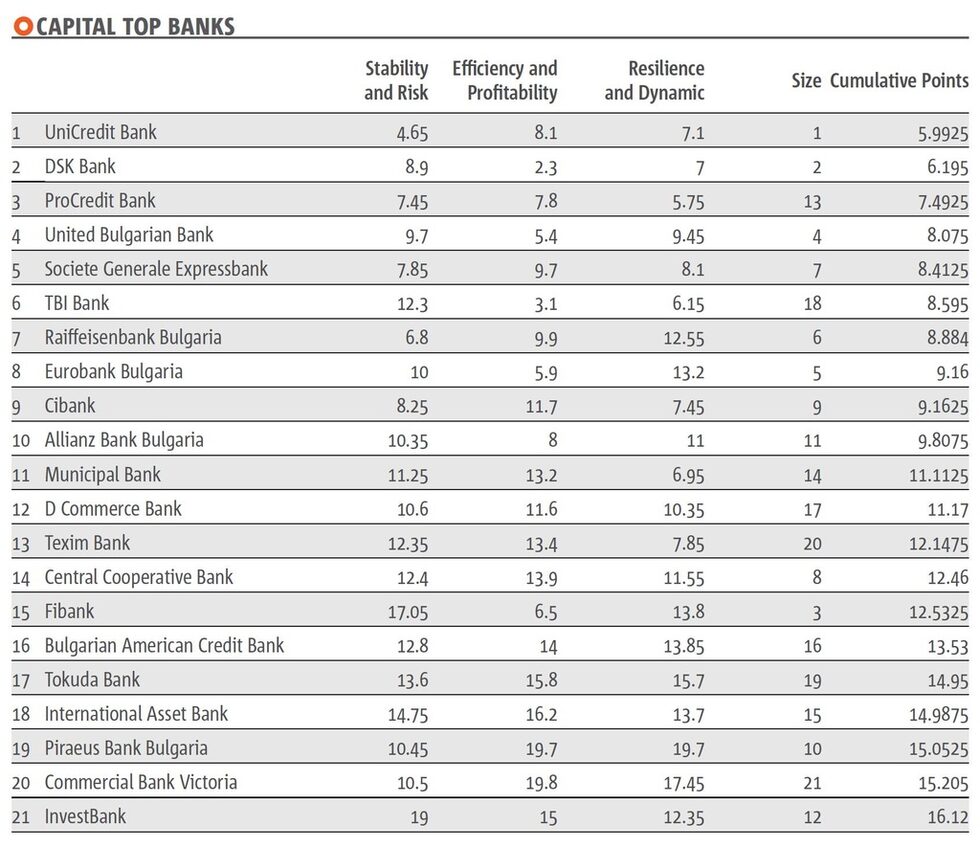

А two-speed banking sector

The Bulgarian banking sector is divided into two groups - banks owned by foreign parents and banks with domestic ownership. The ten best banks in the country remain those that are part of European financial groups, while the second half of the ranking is populated almost entirely by institutions controlled by local business groups.

UniCredit Bulbank is leader for a second year in a row. The bank traditionally builds on its strong performance in the Stability and Risk category in the TOP 10 Banks ranking by Capital newspaper (K10). The largest bank in the country operates with a significant capital surplus, and as at end-2016 its capital adequacy ratio was 27.5% - well above the sector average of 20.9%.

The runner-up in the sixth annual edition of the ranking is DSK Bank, owned by Hungary's OTP Bank. Its big retail portfolio with good interest revenues and economies of scale allow it to maintain a very high cost-to-revenue ratio, making it the most efficient Bulgarian bank.

The third category in Capital's TOP 10 Banks ranking - Resilience and Dynamics, is headed by ProCredit Bank which places it in the third place in the overall ranking.

Excellent results - based on one-off events

In 2016, banks reported a combined profit of BGN 1.26 billion - close to the record levels reached before the crisis year 2008. However, the good results are mainly due to one-off effects and factors that are unlikely to repeat themselves in 2017.

About half of the reported 40% profit growth comes from Visa Inc.' buyback of Visa Europe. The European arm of the US credit card company was owned by several European banks. The payment was based on the turnover of each bank in the card operator's payment system. The share of the Bulgarian Visa banks is BGN 186 million.

A second factor that will probably not repeat itself in 2017 is the dwindling cost of the banks' resources. For the greater part of 2016, banks have benefited from the widening, albeit modest, margin between deposit and loan interest rates. In the first months of 2017, this effect has been exhausted and the cost of bank resources has reached the bottom, while the revenues from their credit portfolio continue to decline.

The profits could have been even stronger, but the banks' excessive liquidity has eaten some of them. The growth of lending is not enough to reduce the available cash in the banks' vaults. The only existing option for them is to park those cash piles in the central bank, but unlike normal times, now they have to pay to the Bulgarian National Bank to store them.

At the same time, 2017 may bring another positive development for Bulgarian banks. Thanks to the robust growth of overall economy, the share of non-performing loans is falling, while the rise in property prices allows banks to sell the collaterals collected over the years. This will reduce the write-downs on banks' bad assets and will boost profits.

Consolidation unlocked

At the beginning of 2016, Postbank acquired the Bulgarian branch of Greece's Alpha Bank. The Greek marriage (Postbank is owned by Greece's Eurobank Ergasias) paved the way for new deals. At the very end of the same year, Belgium's KBC, which already owns Bulgaria's Cibank, acquired United Bulgarian Bank (UBB), owned by National Bank of Greece. This is the largest such deal in Bulgaria in over 10 years after UniCredit Bulbank merged with Biochim Bank and Hebros Bank.

Both of last year's deals were driven by the financial troubles of Greek banks at home - with the result being consolidation of Bulgaria's overcrowded banking sector. The planned merger of UBB and Cibank will create the third biggest bank in Bulgaria by assets, while Eurobank (as Postbank is officially known in Bulgaria) solidified its fifth position in the ranking.

The price of EUR 610 million of the sale of UBB (in bundle with leasing company Interlease) is a good evaluation of the Bulgarian banking market. This will probably attract fresh interest from prospective buyers who are now flush with cash but have few options to invest. There is a number of small players in the Bulgarian banking sector which have a hard time to compete and might pose systemic risks. They are ripe for acquisition.

Bankers expect new deals, though not necessarily in the near future. First Investment Bank (Fibank) has already announced it is looking for new investors who could possibly acquire a majority stake. Two other banks are on the table, too. The trustees of bankrupt Corporate Commercial Bank are looking for an investor who could take over Victoria Bank (formerly Credit Agricole Bulgaria). Victoria was acquired shortly before Corporate Commercial Bank collapsed. The other bank is Tokuda, whose Japanese owner has been trying to find a buyer for a long time.

The customer rules

Еvery banker always says that their most important asset is the client. With more and more non-bank rivals that try to conquer a share of traditional banks' realms, this principle has come to be more of a survival tool, rather than a mere PR stunt. In the last few years, digitization and online services have become a necessity that requires constant efforts to keep up with technological innovations and the customers' expectations. The bank branch has not lost its functions yet, but there are already clients who enter it only as an exception. And they are willing to change their bank because another one offers a more functional mobile banking application.

This process is gaining speed slowly, yet in 2016 several banks already introduced automatic opening of accounts when the money was transferred from another bank, some banks drastically reduced their fees for transfers from abroad, while ProCreditBank expands its individual off-line customer zone.

Capital's TOP 10 Banks ranks the banks according to a number of indicators, which are divided into four categories: stability and risk, efficiency and profitability, resilience and dynamics, and size. The ranking tries not to put too much value on indicators that depend on the size of the bank (asset size, deposits, credits) and those that banks have regulatory or marketing incentives to doctor (bad credit, net profit, equity ratios).

Nearly three years after the dramatic collapse of Corporate Commercial Bank (the fourth biggest bank in Bulgaria in 2014) and the liquidity crisis that threatened the stability of Fibank (the third biggest bank), it can be safely declared that the Bulgarian banking sector has returned to a healthy calm. Bank profits are up, the consolidation of the financial institutions continues, while bank lending rates are steadily converging to the Central European levels.